From semiconductors to software, Carmignac Portfolio Tech Solutions has delivered strong returns since launch by investing across the full technology value chain. This highlights the importance of selectivity in an increasingly polarised market.

Launched in June 2024, at the peak of the so-called “Magnificent 7” era—when the seven mega-cap technology stocks accounted for nearly 80% of the S&P 500’s returns— Carmignac Portfolio Tech Solutions was designed to capture the accelerating adoption of artificial intelligence (AI) and the broad investment cycle supporting it. Rather than focusing on a narrow set of mega-cap AI winners, the strategy was designed to capture innovation across the entire ecosystem, from upstream materials to downstream applications, reflecting a conviction that technological disruption extends far beyond traditional sector boundaries.

Strong early outperformance has reflected this deliberate positioning away from index concentration and towards underappreciated segments of the technology value chain combined with a disciplined approach to valuation.

Since launch, the fund has delivered robust absolute and relative performance (+92.9% vs +74.1%1), outperforming its reference indicator2. In 2025 alone, the fund returned +29.4% compared with +14.8% for its benchmark, placing it in the first quartile of its peer group since inception.

What worked: Monetising the AI capex cycle

The Fund’s performance has been rooted in the strategy’s ability to identify opportunities across the full breadth of the AI ecosystem. Over the past two years, the AI investment theme has evolved from a GPU-led story into a full-stack infrastructure build-out spanning compute, networking, storage, power, cooling and software.

| BROADCOM | MICROSOFT |

| TSMC | ATLASSIAN |

| SK HYNIX | SALESFORCE |

| NVIDIA | GITLAB |

| ALPHABET | SERVICENOW |

Core AI infrastructure

The mission-critical bottlenecks, these companies without which AI training and inference simply cannot scale, have been core holdings of the portfolio since launch and have been among the strategy’s strongest performers.

TSMC has ranked among the top three holdings since day one, reflecting its pivotal role in the AI ecosystem. Building a leading-edge logic foundry from scratch requires decades of process expertise, materials science know-how, and deep relationships across the semiconductor supply chain—capabilities that cannot be replicated quickly. TSMC’s competitive moat strengthens with each successive node generation.

Beyond TSMC, companies such as Nvidia, SK Hynix and Broadcom, among the primary beneficiaries of surging demand for advanced semiconductors—have also been major contributors to performance.

AI Infrastructure buildout, networking and interconnects

The Fund also benefited from its positioning in industrial technology and digital infrastructure, particularly as the AI investment theme broadened. Each new generation of AI systems requires more networking, power infrastructure, cooling capacity, advanced packaging, and specialised materials. As a result, an increasing share of value is accruing to the critical bottlenecks that determine the speed and scale of deployment.

Holdings such as Amphenol, Celestica, and Comfort Systems contributed meaningfully, an area whose importance is often overlooked by traditional sector classifications, despite being essential to the industry's expansion.

The Hidden Enablers Driving Value Creation

Beyond the obvious winners, the strategy also captured value in less visible parts of the supply chain. Companies involved in electronic components and materials, such as those producing copper-clad laminates, delivered outsized returns as demand for AI infrastructure expanded rapidly. Exposure to companies such as Elite Materials and Nitto Boseki illustrates the strategy’s ability to identify off-benchmark beneficiaries of the AI cycle (e.g. laminates, substrates, connectivity components).

This reflects a deliberate effort to monetise second-order effects of AI capex rather than focusing solely on front-end beneficiaries.

Far from being a peripheral player, Asia is the essential enabler of the AI revolution, a reality that investors cannot afford to overlook. While some critical nodes, such as TSMC, are well-known and strategically critical, other companies are far less visible to investors, controlled by a handful of mid-sized firms producing key components. These businesses often combine underappreciated profitability with robust balance sheets, enabling them to capture a compelling growth trajectory and sustained earnings expansion. Emerging market exposure accounts for 43% of the performance of the strategy (vs 19% for the index)3.

Valuation discipline as an alpha driver

A key differentiator has been the integration of valuation discipline within a growth-oriented universe. This approach has been particularly relevant in an environment where parts of the AI ecosystem have experienced rapid multiple expansion disconnected from fundamentals.

Carmignac Portfolio Tech Solutions has sought to monetise this dispersion through a disciplined valuation framework, applied across the investment universe.

The portfolio has been actively managed, with several key actions contributing to performance:

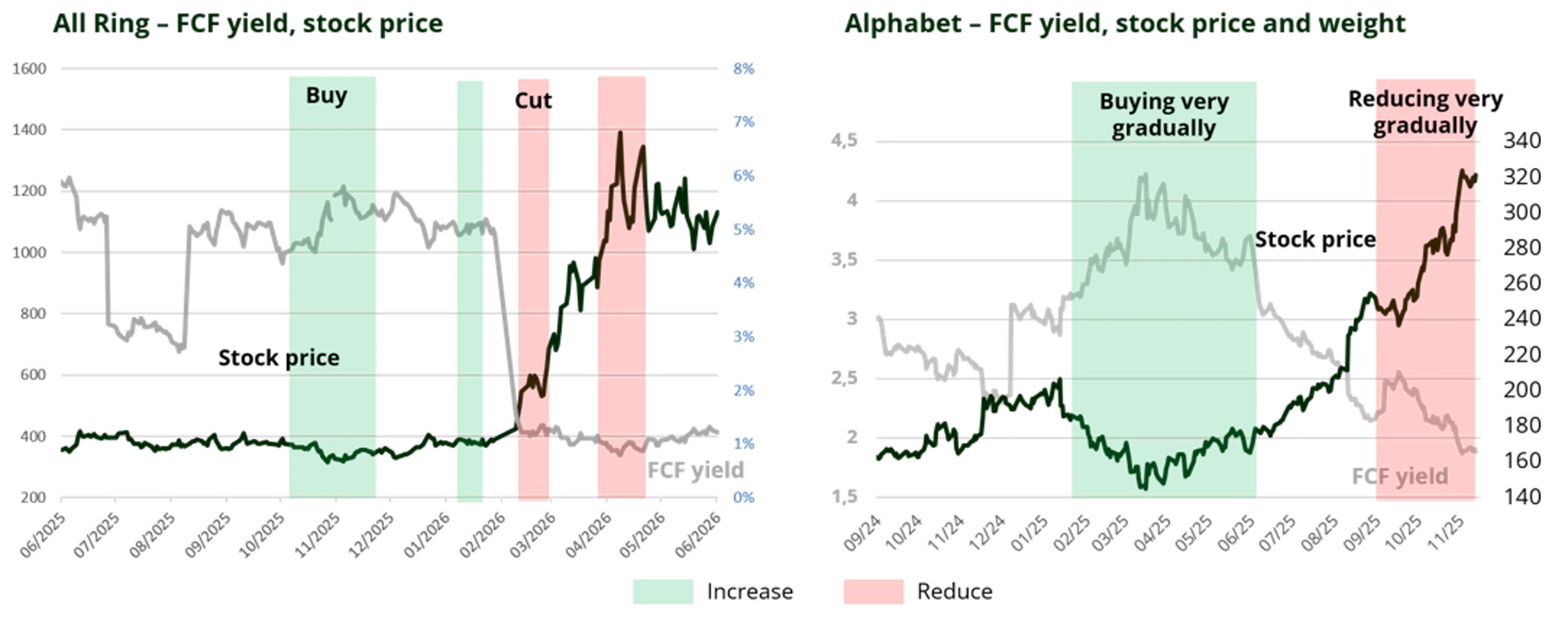

- Capitalizing on the opportunities created by Liberation Day: We actively added to positions during the market weakness in April 2025 and subsequently took profits as markets recovered later in 2025. This disciplined approach was a significant contributor to the portfolio's strong outperformance relative to its benchmark.

- Adjusting exposure to hyperscalers: Over recent months, investor focus has shifted from the scale of AI-related investments to the sustainability of the returns these investments can generate, leading to increased volatility across the sector. In response, we selectively reduced our exposure.

- Actively managing semiconductor portfolio beta: Following the sharp re-rating of semiconductor valuations in 2026, we rebalanced the portfolio by rotating from higher-beta semiconductor names into higher-quality companies with more attractive risk-adjusted return profiles.

The cost of conviction: What did not work

Not all parts of the portfolio contributed positively. Software exposure detracted from performance over 2026, as parts of the market grew concerned that AI would disrupt incumbent business models. These positions had been mostly built at the end of 2025/ beginning of 2026, on the contrarian view that the disruption wave would remain limited for some of the well-established players. We have reduced some of these positions lately, as skepticism toward the segment may persist until markets gain better visibility on the true scale and timing of any disruption.

Positioning: A differentiated way to play technology

Markets remain largely momentum-driven, with narrow leadership and signs of excess in parts of the market, particularly among smaller names that have doubled or tripled in recent months despite unclear fundamentals. That said, the broader picture remains reassuring: the MSCI IT index trades at around 22x P/E, about 10% below its five-year average4 and well below dot-com bubble levels, while recent share-price gains have been driven more by earnings than multiple expansion. The market is also already discounting a moderation in growth next year.

In this environment, selectivity is critical: across all tech segments, we have shifted towards high-quality stocks that offer a valuation safety net, like Nvidia and Broadcom.

Beyond this near-term caution, we believe the medium-term outlook remains robust. The cycle appears to be extending rather than peaking, with companies increasingly planning capacity around 2027–28 demand and signing three-to-five-year supply agreements. AI demand is becoming more additive than cyclical, as edge AI, agentic AI, and physical AI create new compute endpoints while infrastructure deployment remains constrained. This means demand is not simply shifting from one chip generation to the next: each generation is likely to serve a growing base of use cases and customers. As an example, demand for Nvidia’s current Blackwell AI chip platform could remain strong for longer than usual, even as customers begin to prepare for its next-generation Rubin platform.

At its core, the fund is built on a broad and unconstrained investment universe. The strategy invests across sectors and geographies, with a meaningful allocation to emerging markets (c.30%) and small- and mid-cap companies (c.20%), areas which are often underrepresented in traditional technology benchmarks.

This is reflected in the portfolio’s structure. Compared to its benchmark, the Fund exhibits greater exposure to semiconductors, materials and components, alongside a more diversified geographical footprint, including a strong presence in Taiwan and South Korea.

The early success of Carmignac Portfolio Tech Solutions highlights a key reality of today’s technology market: the opportunity set is broader and more complex than ever.

As AI reshapes industries, the next phase of performance is likely to be driven not by being invested in technology, but by being invested in the right parts of it.

Carmignac Portfolio Tech Solutions has demonstrated that navigating this complexity requires more than exposure. It demands selectivity, flexibility, and a willingness to look beyond the obvious.

1As at 29/05/2026, F EUR Acc Share class. Past performance is not necessarily indicative of future performance.

2MSCI AC World Information Technology 10/40 Capped (EUR) Reinvested net dividends. Converted daily.

3As at 29/05/2026, Portfolio allocation is subject to change without notice.

4Bloomberg, As at 29/05/2026.

Carmignac Portfolio Tech Solutions

Carmignac Portfolio Tech Solutions F EUR ACC

- Recommended minimum investment horizon

- 5 years

- Risk indicator*

- 5/7

- SFDR - Fund Classification**

- Article 9

*Risk Scale from the KID (Key Information Document). Risk 1 does not mean a risk-free investment. This indicator may change over time. **Sustainable Finance Disclosure Regulation (SFDR) 2019/2088. The SFDR classification of the Funds may change over time.

Main risks of the fund

Fees

- Entry costs

- We do not charge an entry fee.

- Exit costs

- We do not charge an exit fee for this product.

- Management fees and other administrative or operating costs

- 1.15% of the value of your investment per year. This estimate is based on actual costs over the past year.

- Performance fees

- 20.00% when the share class overperforms the Reference indicator during the performance period. It will be payable also in case the share class has overperformed the reference indicator but had a negative performance. Underperformance is clawed back for 5 years. The actual amount will vary depending on how well your investment performs. The aggregated cost estimation above includes the average over the last 5 years, or since the product creation if it is less than 5 years.

- Transaction Cost

- 0.35% of the value of your investment per year. This is an estimate of the costs incurred when we buy and sell the investments underlying the product. The actual amount varies depending on the quantity we buy and sell.

Performance

| Carmignac Portfolio Tech Solutions | +40.0 | +29.4 | +6.5 |

| Reference Indicator | +41.1 | +14.8 | +7.5 |

| Carmignac Portfolio Tech Solutions | +85.7% | +0.0% | +40.4% |

| Reference Indicator | +73.9% | +0.0% | +33.1% |

Source: Carmignac at 29 May 2026.

Past performance is not necessarily indicative of future performance. Performances are net of fees (excluding possible entrance fees charged by the distributor). The Fund presents a risk of loss of capital.

Reference Indicator: MSCI AC World Information Technology 10/40 Capped NR index

Marketing communication. Please refer to the KID/KIID, prospectus of the fund before making any final investment decisions. This document is intended for professional clients.

This material may not be reproduced, in whole or in part, without prior authorisation from the Management Company. This material does not constitute a subscription offer, nor does it constitute investment advice. This material is not intended to provide, and should not be relied on for, accounting, legal or tax advice. This material has been provided to you for informational purposes only and may not be relied upon by you in evaluating the merits of investing in any securities or interests referred to herein or for any other purposes. The information contained in this material may be partial information and may be modified without prior notice. They are expressed as of the date of writing and are derived from proprietary and non-proprietary sources deemed by Carmignac to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by Carmignac, its officers, employees or agents.

Past performance is not necessarily indicative of future performance. Performances are net of fees (excluding possible entrance fees charged by the distributor). The return may increase or decrease as a result of currency fluctuations, for the shares which are not currency-hedged.

Reference to certain securities and financial instruments is for illustrative purposes to highlight stocks that are or have been included in the portfolios of funds in the Carmignac range. This is not intended to promote direct investment in those instruments, nor does it constitute investment advice. The Management Company is not subject to prohibition on trading in these instruments prior to issuing any communication. The portfolios of Carmignac funds may change without previous notice. The reference to a ranking or prize, is no guarantee of the future results of the UCIS or the manager.

Morningstar Rating™ : © Morningstar, Inc. All Rights Reserved. The information contained herein: is proprietary to Morningstar and/or its content providers; may not be copied or distributed; and is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information.

Access to the Funds may be subject to restrictions regarding certain persons or countries. This material is not directed to any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the material or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not access this material. Taxation depends on the situation of the individual. The Funds are not registered for retail distribution in Asia, in Japan, in North America, nor are they registered in South America. Carmignac Funds are registered in Singapore as restricted foreign scheme (for professional clients only). The Funds have not been registered under the US Securities Act of 1933. The Funds may not be offered or sold, directly or indirectly, for the benefit or on behalf of a «U.S. person», according to the definition of the US Regulation S and FATCA.

The risks, fees and ongoing charges are described in the KID (Key Information Document). The KID must be made available to the subscriber prior to subscription. The subscriber must read the KID. Investors may lose some or all their capital, as the capital in the funds are not guaranteed. The Funds present a risk of loss of capital.

The Funds’ prospectus, KIDs, NAVs and annual reports are available at www.carmignac.com/en, or upon request to the Management Carmignac Portfolio refers to the sub-funds of Carmignac Portfolio SICAV, an investment company under Luxembourg law, conforming to the UCITS Directive. The French investment funds (fonds communs de placement or FCP) are common funds in contractual form conforming to the UCITS or AIFM Directive under French law.

In the United Kingdom: the Funds’ respective prospectuses, KIIDs and annual reports are available at www.carmignac.com/en-gb, or upon request to the Management Company, or for the French Funds, at the offices of the acilities Agent, Carmignac UK Ltd, 2 Carlton House Terrace, London, SW1Y 5AF. This document was prepared by Carmignac Gestion, Carmignac Gestion Luxembourg or Carmignac UK Ltd. FP Carmignac ICVC (the “Company”) is an Investment Company with variable capital incorporated in England and Wales under registered number 839620 and is authorised by the FCA with effect from 4 April 2019 and launched on 15 May 2019. FundRock Partners Limited is the Authorised Corporate Director (the “ACD”) of the Company and is authorised and regulated by the FCA. Registered Office: Hamilton Centre, Rodney Way, Chelmsford, Essex, CM1 3BY, UK; Registered in England and Wales with number 4162989. Carmignac Gestion Luxembourg SA has been appointed as the Investment Manager and distributor in respect of the Company. Carmignac UK Ltd (Registered in England and Wales with number 14162894) has been appointed as a sub-Investment Manager of the Company and is authorised and regulated by the Financial Conduct Authority with FRN:984288.

In Switzerland: the prospectus, KIDs and annual report are available at www.carmignac.com/en-ch, or through our representative in Switzerland, CACEIS (Switzerland), S.A., Route de Signy 35, CH-1260 Nyon. The paying agent is CACEIS Bank, Montrouge, Nyon Branch / Switzerland, Route de Signy 35, 1260 Nyon.

In Belgium: This document is intended for professional clients. This content has not been validated by FSMA. The decision to invest in the promoted fund should take into account all its characteristics or objectives as described in its prospectus. This communication is published by Carmignac Gestion S.A., a portfolio management company approved by the Autorité des Marchés Financiers (AMF) in France, and its Luxembourg subsidiary Carmignac Gestion Luxembourg, S.A., an investment fund management company approved by the Commission de Surveillance du Secteur Financier (CSSF). “Carmignac” is a registered trademark. “Investing in your Interest” is a slogan associated with the Carmignac trademark. This document does not constitute advice on any investment or arbitrage of transferable securities or any other asset management or investment product or service. The information and opinions contained in this document do not take into account investors’ specific individual circumstances and must never be interpreted as legal, tax or investment advice. The information contained in this document may be partial and could be changed without notice. This document may not be reproduced in whole or in part without prior authorisation. The risks and fees are described in the KID (Key Information Document). The prospectus, KID, the net asset-values and the latest (semi-) annual management report may be obtained, free of charge, in French or in Dutch, from the management company (tel. +352 46 70 60 1) or by consulting its website or www.fundinfo.com. These materials may also be obtained from Caceis Belgium S.A., the financial service provider in Belgium, at the following address: avenue du port, 86c b320, B-1000 Brussels. The Fund (fonds commun de placement or FCP) is a common fund in contractual form conforming to the UCITS Directive under French law. Access to the Fund may be subject to restrictions regarding certain persons or countries. The Funds are not registered for retail distribution in Asia, in Japan, in North America, nor are they registered in South America. Carmignac Funds are registered in Singapore as restricted foreign scheme (for professional clients only). The Funds have not been registered under the US Securities Act of 1933. The Funds may not be offered or sold, directly or indirectly, for the benefit or on behalf of a «U.S. person», according to the definition of the US Regulation S and FATCA. In case of subscription to a fund subject to Article 19bis of the Belgian Income Tax Code (CIR92), the investor will have to pay, upon redemption of his or her shares, a withholding tax of 30% on the income (in the form of interest, or capital gains or losses) derived from the return on assets invested in debt claims. Distributions are subject to withholding tax of 30% without income distinction. In case of subscription in a French investment fund (fonds commun de placement or FCP), you must declare on tax form, each year, the share of the dividends (and interest, if applicable) received by the Fund. Any complaint may be referred to complaints@carmignac.com or CARMIGNAC GESTION - Compliance and Internal Controls - 24 place Vendôme Paris France or on the website www.ombudsfin.be.

The Management Company can cease promotion in your country anytime. Investors have access to a summary of their rights at section 5 entitled "summary of investor rights" on the following links: UK ; Switzerland ; France ; Luxembourg ; Sweden. Belgium (French) ; Belgium (Dutch)

For Carmignac Portfolio Long-Short European Equities: Carmignac Gestion Luxembourg SA in its capacity as the Management Company for Carmignac Portfolio, has delegated the investment management of this Sub-Fund to White Creek Capital LLP (Registered in England and Wales with number OCC447169) from 2nd May 2024. White Creek Capital LLP is authorised and regulated by the Financial Conduct Authority with FRN : 998349.

Carmignac Private Evergreen refers to the Private Evergreen sub-fund of the SICAV Carmignac S.A. SICAV – PART II UCI, registered with the Luxembourg RCS under number B285278.