Takeaways from the 2025 voting season

The Annual General Meeting (AGM) season is a key moment in the active asset manager’s calendar: a time for shareholders to have their say and the management of corporates to gauge their investors’ priorities.

The 2025 AGM season unfolded amid evolving government policies, market turbulence and increasing sustainability regulation in both Europe and the US. This vital forum has provided illuminating insights into the shifting state of play between corporates and investors.

Shareholder oversight under threat

The number of resolutions filed by shareholders at US companies declined 30% in 2025 compared to last year1. This was largely influenced by the stricter stance taken by the US Securities and Exchange Commission, as well as a shift in many asset managers’ approach to Environmental, Social and Governance (ESG) issues and voting. We had grown increasingly concerned about the misuse of shareholder resolutions by some investors and commend ‘resolution rationality’. But unfortunately, this regulatory change has had a direct impact on shareholders’ ability to hold boards to account.

European companies have traditionally been more insulated from shareholder filings, because of share ownership structures and in certain countries, the authority granted to boards to determine whether resolutions are included on AGM agendas. And this AGM season, the ‘fewer-resolutions’ trend was even more pronounced. A notable example was the Dutch activist group Follow This, who are renowned for submitting climate-related resolutions at AGMs of major European oil and gas companies. This year the group chose not to file any resolutions, citing insufficient investor backing2.

Corporate governance withstands the backlash

While the politicisation of ESG, along with the evolution of European and US government policy and regulation, has impacted investors’ and issuers’ approaches to sustainability, corporate governance appears to have bucked the trend.

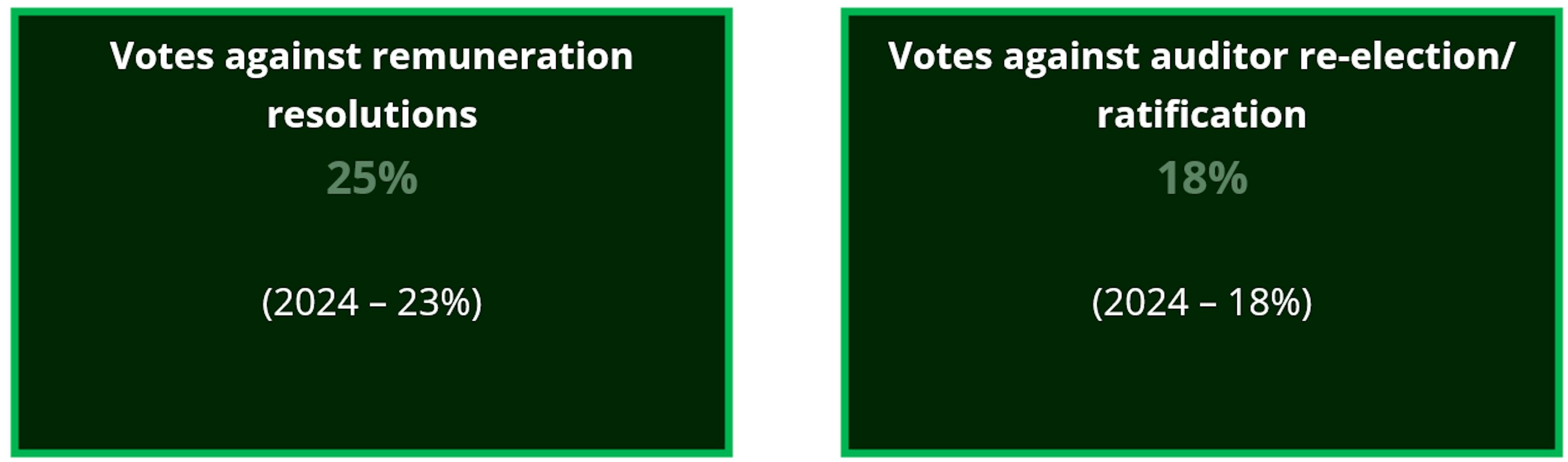

This year there were a considerable number of votes against management on governance topics. For example, at three of the companies held by our portfolios, votes against executive pay reports surpassed 50%3.

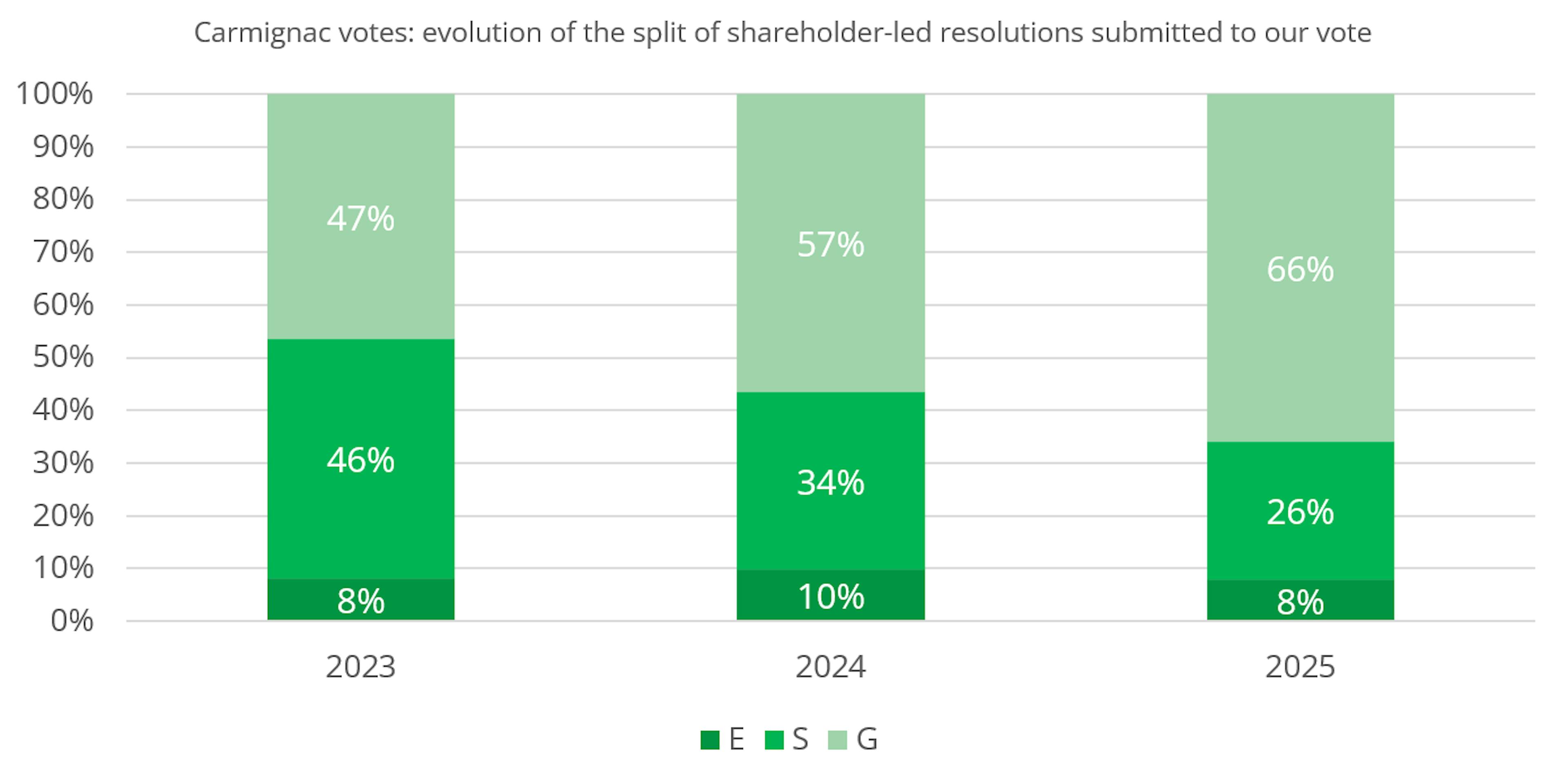

In addition, our data, as evidenced in the chart below, shows more governance shareholder-led resolutions were filed in companies held by our portfolios than resolutions on environmental and social topics.

This trend is confirmed at market-level. According to Morningstar, the volume of environmental and social resolutions decreased by 42% in 2025, compared with a fall of just 6% for governance resolutions4.

Governance shareholder-led resolutions also continue to garner stronger support from shareholders. Although the overall average level of support for shareholder resolutions held steady this year at 23%, Morningstar notes a clear divergence: governance proposals consistently received higher backing than environmental and social ones. This pattern is further reflected in the voting results across our portfolios, where the shareholder-led resolutions that received the highest support levels (exceeding 40%) were governance-focused5. While it remains too early to evaluate the long-term impact, these elevated support levels highlight a continued interest in governance best practice among investors.

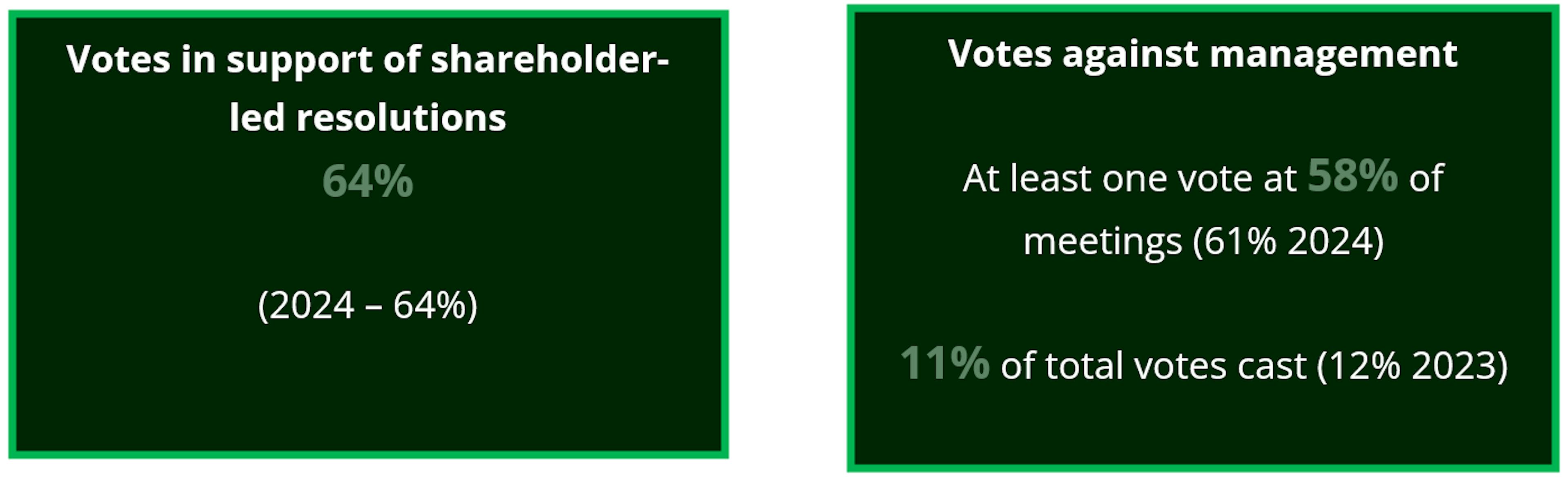

The quality of the governance resolutions brought forward to a vote is also apparent from Carmignac’s records. While our overall backing of shareholder-led resolutions remained high at 64% (70% when excluding ‘anti-ESG’6 resolutions) our highest area of support was governance7.

The positive reach and influence that shareholder-led resolutions can have was recently illustrated when Meta, a controlled technology company, responded to a shareholder vote at its 2024 AGM by amending its corporate governance guidelines. These amendments strengthened the role of the lead director on the board, granting them approval authority over board meeting agenda items. The resolution was initially opposed by management and received support from only 17% of shareholders, including Carmignac, yet it still prompted a structural governance change.

The new era of AGMs has brought renewed focus to corporate governance but minority shareholder rights remain vulnerable, especially given debates surrounding European market competitiveness. A recent example is the strong shareholder backing for the payments company, Wise’s decision to shift its primary listing from the UK to the US, despite the continuation of a controversial dual-class share structure and the dilution of governance standards, both of which negatively affect minority shareholder protections. Therefore, Carmignac voted against all resolutions at the shareholder meeting held on 28th July.

Carmignac’s constant voting stance in changing times

While the landscape is changing, we’ve remained steadfast in our voting approach and in holding corporate management teams to account on ESG issues. We share our key statistics below.

1Morningstar, The 2025 Proxy Season in 7 Charts, 25 July 2025.

2Follow This, Press Release, 10 April 2025; https://www.follow-this.org/follow-this-pauses-climate-resolutions-for-big-oil-in-2025-amid-investor-hesitation/.

3Source: Carmignac, using ISS ProxyExchange data.

4Source: Morningstar.

5Source: Carmignac, using ISS Proxy Exchange data.

6Anti-ESG resolutions are resolutions filed by shareholders which are politically motivated against the adoption or implementation of ESG considerations by issuers.

7Note that the data does not include shareholder-led resolutions which we categorise as “anti-ESG” as they skew the data. Our policy is to systematically oppose these resolutions as they are politically motivated.

Articles that may interest you

Quarter 1 2025: Our active stewardship illustrated

Underprepared companies in the crosshairs of physical climate risks

Shareholder meetings: A necessary change of tone

Marketing communication. Please refer to the KID/KIID, prospectus of the fund before making any final investment decisions. This document is intended for professional clients.

This material may not be reproduced, in whole or in part, without prior authorisation from the Management Company. This material does not constitute a subscription offer, nor does it constitute investment advice. This material is not intended to provide, and should not be relied on for, accounting, legal or tax advice. This material has been provided to you for informational purposes only and may not be relied upon by you in evaluating the merits of investing in any securities or interests referred to herein or for any other purposes. The information contained in this material may be partial information and may be modified without prior notice. They are expressed as of the date of writing and are derived from proprietary and non-proprietary sources deemed by Carmignac to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by Carmignac, its officers, employees or agents.

Past performance is not necessarily indicative of future performance. Performances are net of fees (excluding possible entrance fees charged by the distributor). The return may increase or decrease as a result of currency fluctuations, for the shares which are not currency-hedged.

Reference to certain securities and financial instruments is for illustrative purposes to highlight stocks that are or have been included in the portfolios of funds in the Carmignac range. This is not intended to promote direct investment in those instruments, nor does it constitute investment advice. The Management Company is not subject to prohibition on trading in these instruments prior to issuing any communication. The portfolios of Carmignac funds may change without previous notice. The reference to a ranking or prize, is no guarantee of the future results of the UCIS or the manager.

Morningstar Rating™ : © Morningstar, Inc. All Rights Reserved. The information contained herein: is proprietary to Morningstar and/or its content providers; may not be copied or distributed; and is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information.

Access to the Funds may be subject to restrictions regarding certain persons or countries. This material is not directed to any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the material or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not access this material. Taxation depends on the situation of the individual. The Funds are not registered for retail distribution in Asia, in Japan, in North America, nor are they registered in South America. Carmignac Funds are registered in Singapore as restricted foreign scheme (for professional clients only). The Funds have not been registered under the US Securities Act of 1933. The Funds may not be offered or sold, directly or indirectly, for the benefit or on behalf of a «U.S. person», according to the definition of the US Regulation S and FATCA.

The risks, fees and ongoing charges are described in the KID (Key Information Document). The KID must be made available to the subscriber prior to subscription. The subscriber must read the KID. Investors may lose some or all their capital, as the capital in the funds are not guaranteed. The Funds present a risk of loss of capital.

The Funds’ prospectus, KIDs, NAVs and annual reports are available at www.carmignac.com/en, or upon request to the Management Carmignac Portfolio refers to the sub-funds of Carmignac Portfolio SICAV, an investment company under Luxembourg law, conforming to the UCITS Directive. The French investment funds (fonds communs de placement or FCP) are common funds in contractual form conforming to the UCITS or AIFM Directive under French law.

In the United Kingdom: the Funds’ respective prospectuses, KIIDs and annual reports are available at www.carmignac.com/en-gb, or upon request to the Management Company, or for the French Funds, at the offices of the acilities Agent, Carmignac UK Ltd, 2 Carlton House Terrace, London, SW1Y 5AF. This document was prepared by Carmignac Gestion, Carmignac Gestion Luxembourg or Carmignac UK Ltd. FP Carmignac ICVC (the “Company”) is an Investment Company with variable capital incorporated in England and Wales under registered number 839620 and is authorised by the FCA with effect from 4 April 2019 and launched on 15 May 2019. FundRock Partners Limited is the Authorised Corporate Director (the “ACD”) of the Company and is authorised and regulated by the FCA. Registered Office: Hamilton Centre, Rodney Way, Chelmsford, Essex, CM1 3BY, UK; Registered in England and Wales with number 4162989. Carmignac Gestion Luxembourg SA has been appointed as the Investment Manager and distributor in respect of the Company. Carmignac UK Ltd (Registered in England and Wales with number 14162894) has been appointed as a sub-Investment Manager of the Company and is authorised and regulated by the Financial Conduct Authority with FRN:984288.

In Switzerland: the prospectus, KIDs and annual report are available at www.carmignac.com/en-ch, or through our representative in Switzerland, CACEIS (Switzerland), S.A., Route de Signy 35, CH-1260 Nyon. The paying agent is CACEIS Bank, Montrouge, Nyon Branch / Switzerland, Route de Signy 35, 1260 Nyon.

The Management Company can cease promotion in your country anytime. Investors have access to a summary of their rights in English on the following links: UK ; Switzerland ; France ; Luxembourg ; Sweden.

For Carmignac Portfolio Long-Short European Equities: Carmignac Gestion Luxembourg SA in its capacity as the Management Company for Carmignac Portfolio, has delegated the investment management of this Sub-Fund to White Creek Capital LLP (Registered in England and Wales with number OCC447169) from 2nd May 2024. White Creek Capital LLP is authorised and regulated by the Financial Conduct Authority with FRN : 998349.

Carmignac Private Evergreen refers to the Private Evergreen sub-fund of the SICAV Carmignac S.A. SICAV – PART II UCI, registered with the Luxembourg RCS under number B285278.