Recent years have challenged a widely accepted assumption: the idea of “natural” diversification across asset classes. In 2022, and more recently amid tensions in the Middle East, equities and bonds declined simultaneously, reminding investors that a portfolio may appear diversified… yet still move in lockstep when markets come under stress.

Today, diversification is no longer simply about allocating between equities and bonds. Many assets now react similarly to common drivers such as inflation expectations, monetary policy shifts, and growth outlooks. In this context, effective diversification requires a more demanding approach: combining genuinely differentiated sources of return that can withstand a range of market environments. These are the principles that guide our diversification strategy within the Carmignac Patrimoine Fund.

Safe-Haven Assets Are Not Infallible

The defensive nature of a so-called “safe haven” asset works under certain economic conditions. In other words, no asset provides permanent protection, it all depends on how investors are positioned within the macroeconomic environment. As these conditions evolve, so too does the behaviour of safe-haven assets.

Gold: A Changing Safe Haven

Traditionally seen as the ultimate safe-haven asset, gold has deviated from this role in recent years.

Following a solid 2024 and an exceptional 2025 (+64%1), gold entered a near-parabolic phase at the start of 2026.

As a non-industrial asset with an inconsistent relationship to both inflation and the economic cycle, gold lends itself to a wide range of narratives: de-dollarisation, fiscal slippage, geopolitical fragmentation, or even more exogenous factors. In this environment, the yellow metal has at times behaved more like a growth asset than a defensive one.

The outbreak of the Iranian conflict reshuffled the deck, triggering a marked decline in gold prices, contrary to its traditional role as a hedge during geopolitical stress. We believe this disconnect can be explained by several concurrent factors: highly crowded positioning, significant profit-taking, rising real yields, and reduced support from Middle Eastern central banks. These developments highlight the increasingly complex role of gold in portfolios, particularly when valuations become stretched.

Within Carmignac Patrimoine, we adopt an active approach. For instance, in response to identified momentum risk in gold, we significantly reduced our exposure to gold mining equities from around 3% at the end of 2025 to 0.5% in March 20262.

Rising Yields: A New Source of Risk

Bonds have long been the primary stabilizer in diversified portfolios. However, this paradigm has been fundamentally challenged since 2022, in an environment where the correlation between equities and rates has deteriorated significantly.

Since the outbreak of the Iranian conflict, rising yields have reflected a broader reassessment of inflation and risk premia. The geopolitical shock initially acted as an energy supply shock, driving oil prices higher and increasing supply chain volatility, thereby reigniting inflationary pressures that central banks had not fully anchored. As a result, medium-term inflation expectations have been revised upward, mechanically pushing both real and inflation components of long-term yields higher.

At the same time, this shock comes against the backdrop of already constrained fiscal conditions, with elevated levels of public debt. It has further increased sovereign issuance needs, particularly in Europe, adding additional upward pressure on long-term yields.

This market environment underscores that diversification can no longer rely on supposedly stable structural relationships.

Within Carmignac Patrimoine, modified duration is managed flexibly, ranging from a range of -4 to +10, and represents a genuine source of diversification. At the beginning of 2026, we adopted negative duration to protect the portfolio in an environment of persistent inflation and robust growth, particularly in the United States. This positioning proved effective in March amid the Iran crisis.

Maintaining Independence from Market Consensus

In uncertain environments, market consensus can quickly become a source of risk. Our approach combines exposure to prevailing market trends (“momentum”) with more differentiated convictions derived from our macroeconomic and fundamental analysis.

For example, we maintain meaningful exposure to the technology sector while implementing targeted reallocations. Alongside positions in the semiconductor value chain, we reduced exposure to hyperscalers in favour of software companies, taking advantage of a sharp correction in the segment and what we believe to be excessively pessimistic market expectations relative to fundamentals. Initiated ahead of tensions related to the Iran conflict, this contrarian positioning materialized more quickly than expected, as renewed geopolitical risk accelerated the normalization of overly depressed valuations.

In addition, our conviction that inflation would prove more persistent than markets anticipated led us to incorporate inflation-linked instruments as early as 2024, well before recent geopolitical developments. This positioning aimed to hedge against a repricing of inflation expectations in a context marked by fiscal imbalances, sustained growth, and structural factors such as demographic trends and the reconfiguration of supply chains.

More broadly, this investment discipline reflects our commitment to building robust portfolios capable of withstanding multiple market regimes, avoiding consensus biases, and continuously seeking true sources of diversification.

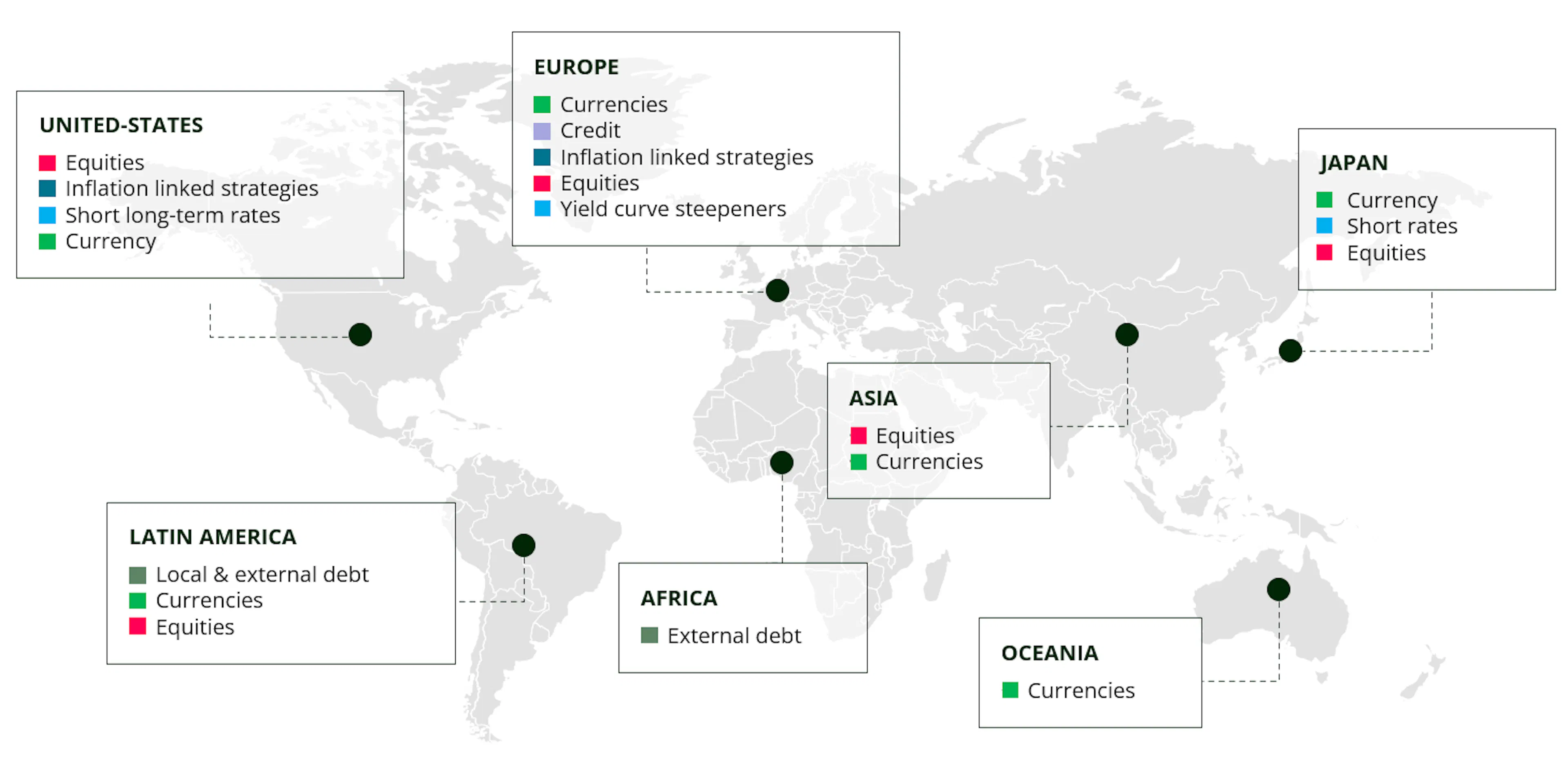

Leveraging Geographic Diversification

Diversification also relies on active geographic allocation. Economic cycles, monetary policies, and sector dynamics vary significantly across regions. Within Carmignac Patrimoine, our allocation goes beyond a static regional split. It is based on a granular assessment of opportunities, enabling us to identify, within each region, the most relevant asset classes to express a given investment theme.

Take commodities as an example. Our scenario of structurally higher inflation supports a constructive allocation to this theme. However, this exposure is not systematically implemented through equities. Instead, we have chosen to express this conviction through currencies of countries we consider closely linked to commodity cycles, such as the Brazilian real and the Australian dollar. This is precisely what geographic diversification means: leveraging the full breadth of market instruments to select the most appropriate vehicles for expressing an investment view.

Buying Protection When It Is Cheap

No one would consider taking out home insurance once their house is already on fire, it would simply be too late. Yet in financial markets, this behavior is common: investors neglect protection in calm periods, only to rush into options during market stress… precisely when they are most expensive and least effective.

Derivatives, and options in particular, can be highly effective provided they are used at the right time and with a clear understanding of their risks. Within Carmignac Patrimoine, the investment team favors their use during periods of low volatility, when we consider risks to be underpriced and the convexity they offer is attractive ; that is, when the trade-off between upfront cost and potential protection is favorable.

These instruments can be deployed across asset classes, including equities, rates, currencies, and volatility, with the aim of limiting the impact of large adverse market movements on portfolio performance.

Case Study: CDS, our 2026 Insurance

1Source: Bloomberg, 31/12/2025.

2Source: Carmignac, as of 27/03/2026.

Carmignac Patrimoine

Carmignac Patrimoine A EUR Acc

- Recommended minimum investment horizon

- 3 years

- Risk indicator*

- 3/7

- SFDR - Fund Classification**

- Article 8

*Risk Scale from the KID (Key Information Document). Risk 1 does not mean a risk-free investment. This indicator may change over time. **Sustainable Finance Disclosure Regulation (SFDR) 2019/2088. The SFDR classification of the Funds may change over time.

Main risks of the fund

Fees

- Entry costs

- 4,00% of the amount you pay in when entering this investment. This is the most you will be charged. Carmignac Gestion doesn't charge any entry fee. The person selling you the product will inform you of the actual charge.

- Exit costs

- We do not charge an exit fee for this product.

- Management fees and other administrative or operating costs

- 1,80% of the value of your investment per year. This estimate is based on actual costs over the past year.

- Performance fees

- 20,00% max. of the outperformance once performance since the start of the year exceeds that of the reference indicator and if no past underperformance still needs to be offset. The actual amount will vary depending on how well your investment performs. The aggregated cost estimation above includes the average over the last 5 years, or since the product creation if it is less than 5 years.

- Transaction Cost

- 0,32% of the value of your investment per year. This is an estimate of the costs incurred when we buy and sell the investments underlying the product. The actual amount varies depending on the quantity we buy and sell.

Performance

| Carmignac Patrimoine | +2,1 | +12,1 | +7,1 | +2,2 | −9,4 | −0,9 | +12,4 | +10,5 | −11,3 | +0,1 |

| Reference Indicator | +2,2 | +1,1 | +11,4 | +7,7 | −10,3 | +13,3 | +5,2 | +18,2 | −0,1 | +1,5 |

| Carmignac Patrimoine | +8,1% | +2,4% | +2,6% |

| Reference Indicator | +6,7% | +4,8% | +5,7% |

Source: Carmignac at Feb 27, 2026.

Past performance is not necessarily indicative of future performance. Performances are net of fees (excluding possible entrance fees charged by the distributor). The Fund presents a risk of loss of capital.

Reference Indicator: 40% MSCI AC World NR index + 40% ICE BofA Global Government index + 20% €STR Capitalized index. Quarterly rebalanced.

Marketing communication. Please refer to the KID/KIID, prospectus of the fund before making any final investment decisions.

This material may not be reproduced, in whole or in part, without prior authorisation from the Management Company. This material does not constitute a subscription offer, nor does it constitute investment advice. This material is not intended to provide, and should not be relied on for, accounting, legal or tax advice. This material has been provided to you for informational purposes only and may not be relied upon by you in evaluating the merits of investing in any securities or interests referred to herein or for any other purposes. The information contained in this material may be partial information and may be modified without prior notice. They are expressed as of the date of writing and are derived from proprietary and non-proprietary sources deemed by Carmignac to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by Carmignac, its officers, employees or agents.

Past performance is not necessarily indicative of future performance. Performances are net of fees (excluding possible entrance fees charged by the distributor). The return may increase or decrease as a result of currency fluctuations, for the shares which are not currency-hedged.

Reference to certain securities and financial instruments is for illustrative purposes to highlight stocks that are or have been included in the portfolios of funds in the Carmignac range. This is not intended to promote direct investment in those instruments, nor does it constitute investment advice. The Management Company is not subject to prohibition on trading in these instruments prior to issuing any communication. The portfolios of Carmignac funds may change without previous notice. The reference to a ranking or prize, is no guarantee of the future results of the UCIS or the manager.

Morningstar Rating™ : © Morningstar, Inc. All Rights Reserved. The information contained herein: is proprietary to Morningstar and/or its content providers; may not be copied or distributed; and is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information.

Access to the Funds may be subject to restrictions regarding certain persons or countries. This material is not directed to any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the material or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not access this material. Taxation depends on the situation of the individual. The Funds are not registered for retail distribution in Asia, in Japan, in North America, nor are they registered in South America. Carmignac Funds are registered in Singapore as restricted foreign scheme (for professional clients only). The Funds have not been registered under the US Securities Act of 1933. The Funds may not be offered or sold, directly or indirectly, for the benefit or on behalf of a «U.S. person», according to the definition of the US Regulation S and FATCA.

The risks, fees and ongoing charges are described in the KID (Key Information Document). The KID must be made available to the subscriber prior to subscription. The subscriber must read the KID. Investors may lose some or all their capital, as the capital in the funds are not guaranteed. The Funds present a risk of loss of capital.

The Funds’ prospectus, KIDs, NAVs and annual reports are available at www.carmignac.com/en, or upon request to the Management Carmignac Portfolio refers to the sub-funds of Carmignac Portfolio SICAV, an investment company under Luxembourg law, conforming to the UCITS Directive. The French investment funds (fonds communs de placement or FCP) are common funds in contractual form conforming to the UCITS or AIFM Directive under French law.

In the United Kingdom: the Funds’ respective prospectuses, KIIDs and annual reports are available at www.carmignac.com/en-gb, or upon request to the Management Company, or for the French Funds, at the offices of the acilities Agent, Carmignac UK Ltd, 2 Carlton House Terrace, London, SW1Y 5AF. This document was prepared by Carmignac Gestion, Carmignac Gestion Luxembourg or Carmignac UK Ltd. FP Carmignac ICVC (the “Company”) is an Investment Company with variable capital incorporated in England and Wales under registered number 839620 and is authorised by the FCA with effect from 4 April 2019 and launched on 15 May 2019. FundRock Partners Limited is the Authorised Corporate Director (the “ACD”) of the Company and is authorised and regulated by the FCA. Registered Office: Hamilton Centre, Rodney Way, Chelmsford, Essex, CM1 3BY, UK; Registered in England and Wales with number 4162989. Carmignac Gestion Luxembourg SA has been appointed as the Investment Manager and distributor in respect of the Company. Carmignac UK Ltd (Registered in England and Wales with number 14162894) has been appointed as a sub-Investment Manager of the Company and is authorised and regulated by the Financial Conduct Authority with FRN:984288.

In Switzerland: the prospectus, KIDs and annual report are available at www.carmignac.com/en-ch, or through our representative in Switzerland, CACEIS (Switzerland), S.A., Route de Signy 35, CH-1260 Nyon. The paying agent is CACEIS Bank, Montrouge, Nyon Branch / Switzerland, Route de Signy 35, 1260 Nyon.

The Management Company can cease promotion in your country anytime. Investors have access to a summary of their rights in English on the following links: UK ; Switzerland ; France ; Luxembourg ; Sweden.

For Carmignac Portfolio Long-Short European Equities: Carmignac Gestion Luxembourg SA in its capacity as the Management Company for Carmignac Portfolio, has delegated the investment management of this Sub-Fund to White Creek Capital LLP (Registered in England and Wales with number OCC447169) from 2nd May 2024. White Creek Capital LLP is authorised and regulated by the Financial Conduct Authority with FRN : 998349.

Carmignac Private Evergreen refers to the Private Evergreen sub-fund of the SICAV Carmignac S.A. SICAV – PART II UCI, registered with the Luxembourg RCS under number B285278.