Fiscal policy takes the driver’s seat

The global economy has entered 2026 in a late-cycle configuration: resilient growth, persistent pockets of inflation, elevated asset valuations, and historically high public deficits. The synchronised monetary easing of the past two years is now giving way to a phase of clear policy divergence. The Federal Reserve (Fed) is on hold, with markets pricing around 50 basis points of easing; the European Central Bank (ECB) and the Bank of England are also on hold, albeit with different biases; the Bank of Japan (BoJ) is cautiously normalising; and the Reserve Bank of Australia delivered a hawkish hike at its February meeting.

At the same time, fiscal policy has re-emerged as the dominant macro force. In the US, the deficit is expected to remain close to 6% of GDP in 20261, while Germany’s fiscal expansion is reshaping euro area growth and supply dynamics.

This shift from monetary to fiscal leadership is altering the nature of risk premia embedded in sovereign yield curves. With structurally higher issuance, inflation not fully extinguished and growing political uncertainty, supply dynamics and term premia are becoming as important as central bank reaction functions. Sovereign bonds can no longer be assessed solely through the prism of policy rates; duration risk increasingly reflects fiscal sustainability, debt absorption capacity, and institutional stability.

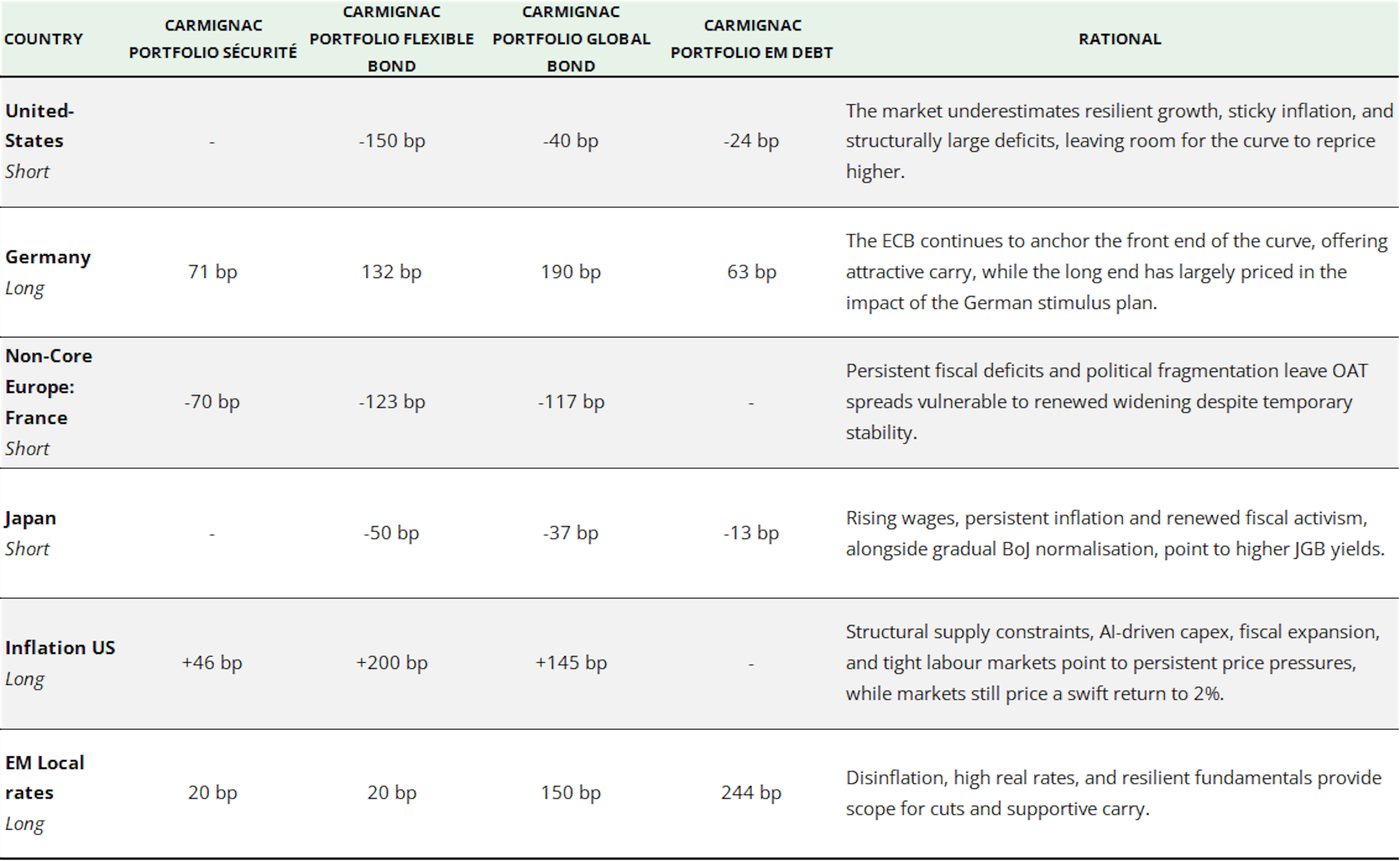

Against this backdrop, we favour differentiated duration exposure: short US and Japan, long Germany, cautious on non-core Europe and constructive on selected emerging markets.

US: Life in the fast lane

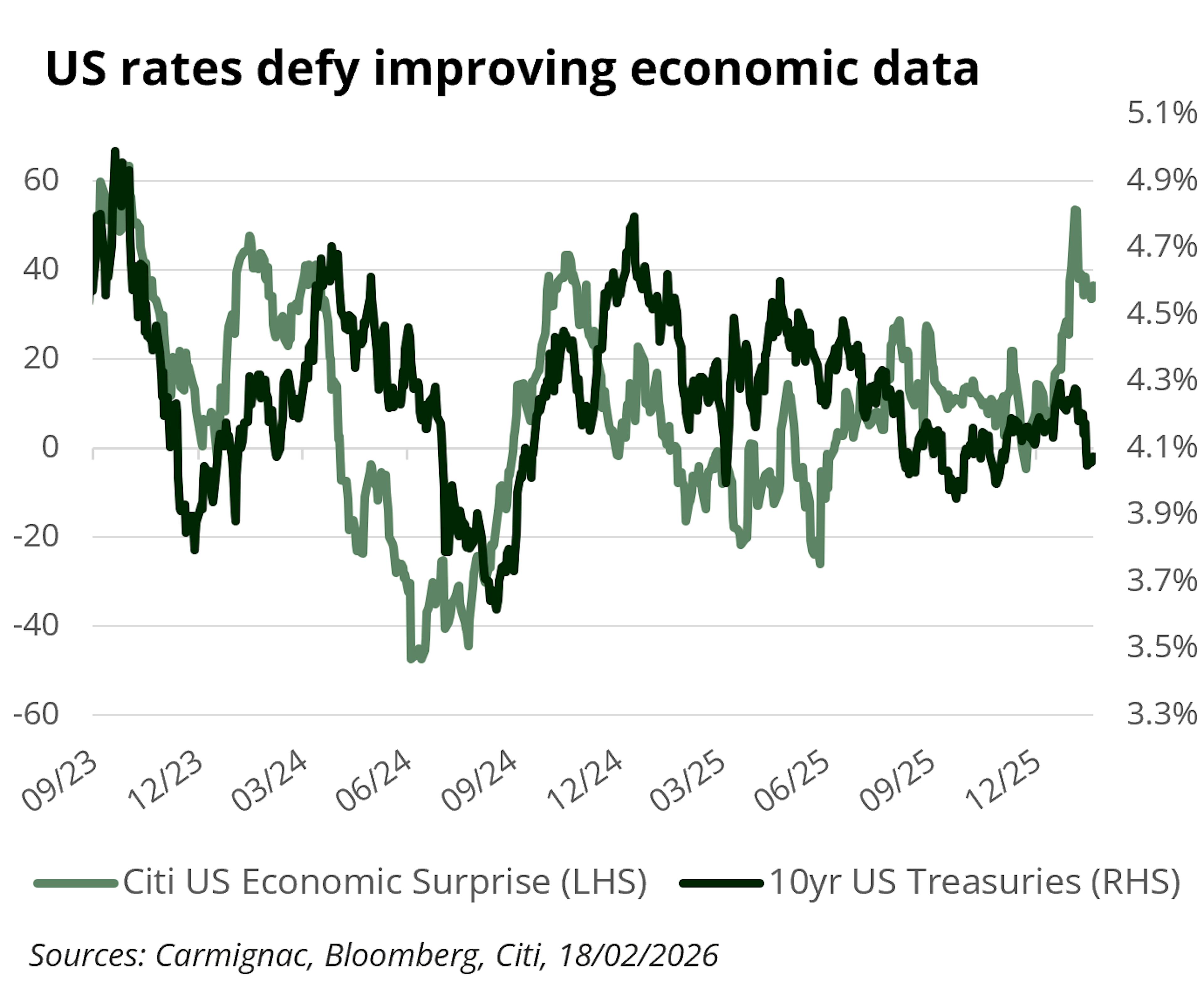

US yields declined in 2025 as recession fears resurfaced and the Fed pivoted toward easing. Yet that rally increasingly appears at odds with underlying fundamentals.

The US economy continues to demonstrate resilience. Leading indicators remain consistent with growth running around 2–2.5% in 2026, supported by AI-driven capital expenditure and the fiscal impulse embedded in the “One Big Beautiful Bill.” The labour market has cooled but not cracked, with unemployment stabilising in the mid-4% range, far from recession territory.

Fiscal gravity, however, cannot be ignored. Recent projections suggest that the 12-month federal deficit-to-GDP ratio could rise from roughly 5.3% at the start of 2026 to around 6.0% by year-end1—well above pre-pandemic norms and roughly double the 2015–2019 average. While this does not signal an imminent fiscal crisis, it confirms that deficits are set to remain structurally large. In nominal terms, this implies continued heavy Treasury issuance. Even if net supply moderates at the front end, long-dated duration remains structurally abundant, particularly at a time when traditional price-insensitive buyers are less dominant.

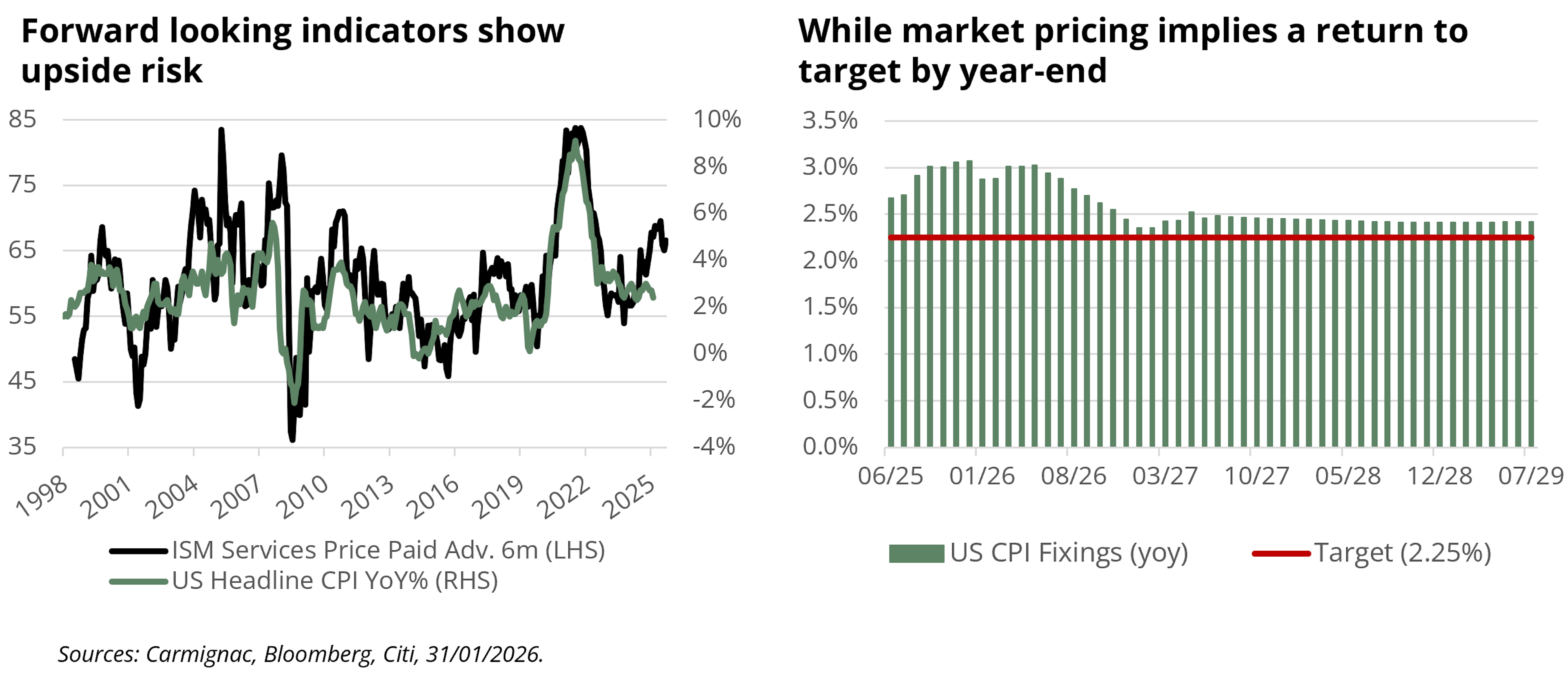

Inflation remains sticky in core components and above the Fed’s target. Core PCE is projected to hover well above 2% in 2026, with risks skewed to the upside. Elevated geopolitical tensions in the Middle East, including recent disruptions around Iran and the Strait of Hormuz, add a further near-term upside risk to energy prices and inflation expectations, even if the persistence of the shock remains uncertain. Against this backdrop, markets are pricing roughly 50 basis points of rate cuts in 2026—an assumption that may prove optimistic if growth holds near trend and fiscal policy remains supportive.

In our view, the bond market is not fully pricing this combination of resilient activity, persistent inflation, and entrenched deficits. With the 10-year Treasury trading around 4%, near the lower end of its recent range, valuations leave room for a repricing. As term premia gradually rebuild and supply remains abundant, the asymmetry for US duration now points toward higher yields across the curve.

Germany: Europe’s fiscal rebound, structural limits

Europe is gradually emerging from stagnation into a more visible cyclical recovery. Germany, long the region’s weak link, has marked a meaningful shift by easing its debt brake and committing up to €500 billion to infrastructure and defence, a move that could add between 0.5% and 1% to annual GDP over the next decade. After a tepid 2025, forward-looking indicators (factory orders, industrial production and credit) are improving, suggesting momentum is building.

This momentum extends beyond Germany. Italy continues to benefit from EU recovery funds, France maintains elevated public spending, and Spain is supported by solid domestic demand and EU financing. Together, this coordinated fiscal stance is sufficient to generate a cyclical upswing, even as private investment and export competitiveness remain structural weaknesses.

We therefore expect euro area growth of around 1.3% in 2026, slightly above consensus. While the upswing is real, modest productivity gains, slow reforms and persistent political fragmentation mean its durability will depend on transforming a fiscally supported rebound into sustainable, private-sector-driven growth.

Inflation, meanwhile, is evolving along a more reassuring path. Price pressures are easing more convincingly than in the US, supported by fading energy effects and a gradual moderation in wage dynamics. This environment places the ECB, in its own words, “in a good place”2. Disinflation is progressing, albeit at a slower pace; labour markets remain resilient; and fiscal expansion reduces the urgency to ease further, while the asymmetry of risks makes additional tightening unlikely.

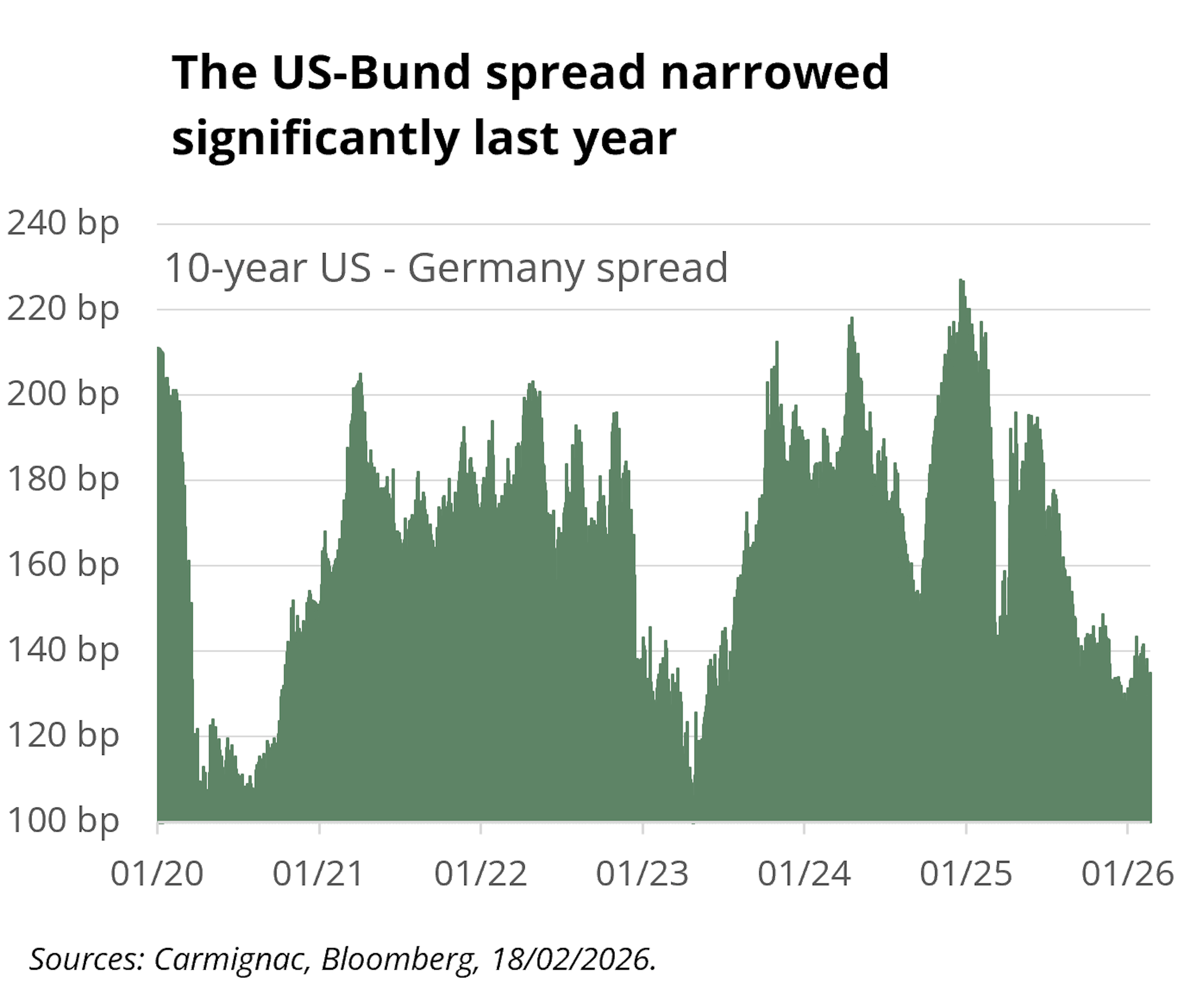

For German rates, the message is clear. The short end of the curve remains firmly anchored by ECB policy, offering attractive carry, the name of the game in a stabilising environment. The long end has already repriced much of the fiscal stimulus, with Bund yields having risen sharply last year. Bunds also retain their safe-haven appeal, particularly as US policy uncertainty clouds the outlook for Treasuries. Our positioning therefore favours the front end of the German curve, where relative value versus the US remains compelling.

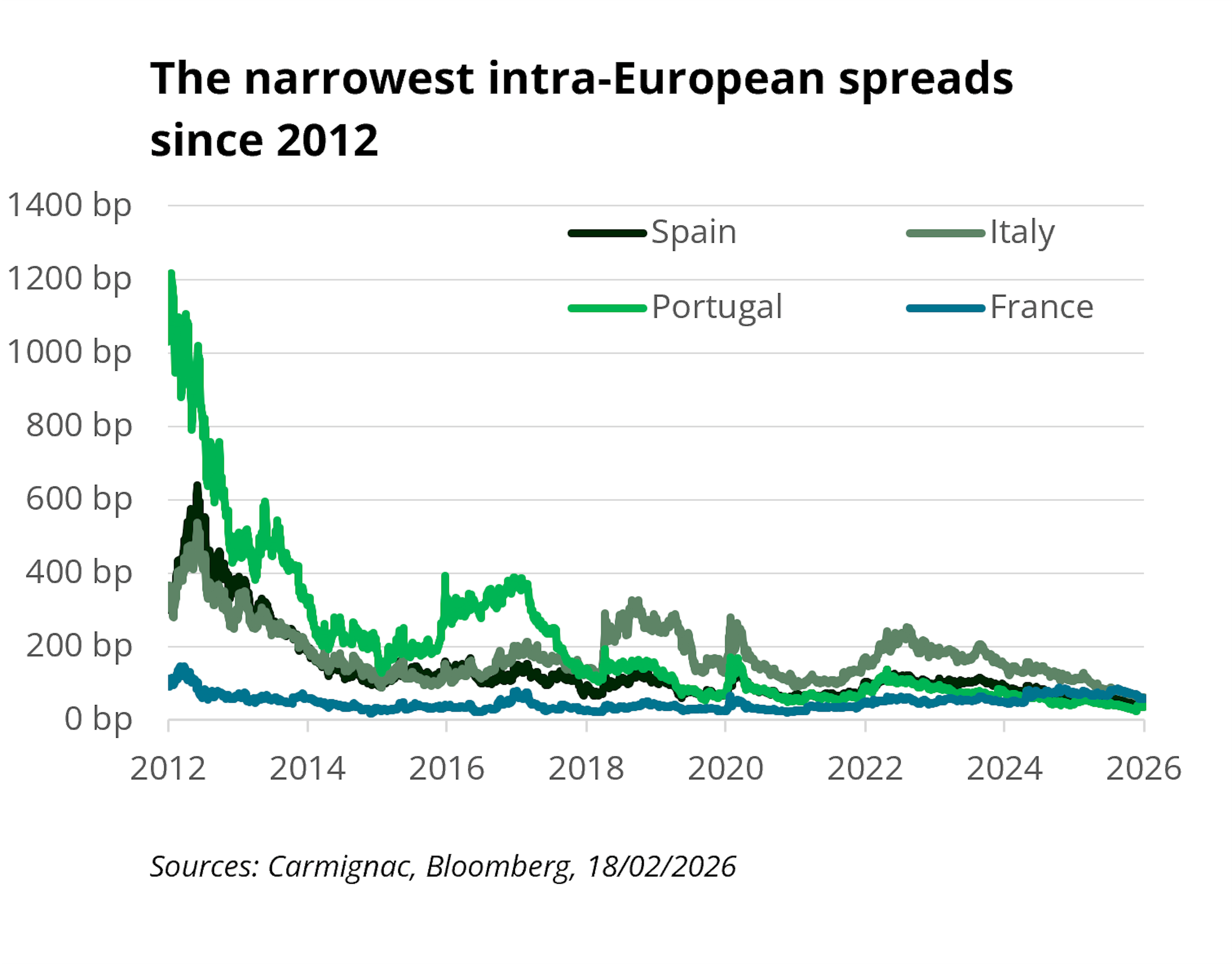

Non-core Europe: Tight spreads, fragile foundations

While Germany stands as the fiscal pillar of the eurozone recovery, the picture is more nuanced elsewhere. The factors underpinning German stability: credible institutions, strong fiscal capacity and safe-haven status, are not uniformly shared across the periphery. Spreads remain historically tight, reflecting a market driven by carry and the search for yield. Yet this environment risks masking underlying fiscal and political vulnerabilities in certain countries, with France standing out as a notable example.

While the passage of the 2026 budget and the failure of subsequent no-confidence motions may temporarily quiet domestic political noise, we believe the respite for OATs3 could prove short-lived. Political fragmentation continues to weigh on confidence, with households maintaining a high savings rate and little inclination to spend. As savings are largely concentrated among pensioners with a low propensity to consume, we believe a meaningful rebound in domestic demand appears unlikely.

Meanwhile, the modest fiscal consolidation planned for 2026, based mainly on selective tax increases and restrained spending, should act as a drag on investment and growth. Persistent uncertainty around the fiscal path risks further dampening private-sector confidence and capital expenditure, widening the gap with more dynamic parts of the euro area. With deficits expected to remain above 5% of GDP and debt exceeding 110%, France remains exposed to renewed rating pressure.

We do not see systemic risk, but we do see fragility. At around 60 basis points versus Bunds—a low since the June 2024 dissolution—spreads offer limited cushion against adverse surprises and could revisit the 70–90 basis points range in negative scenarios.

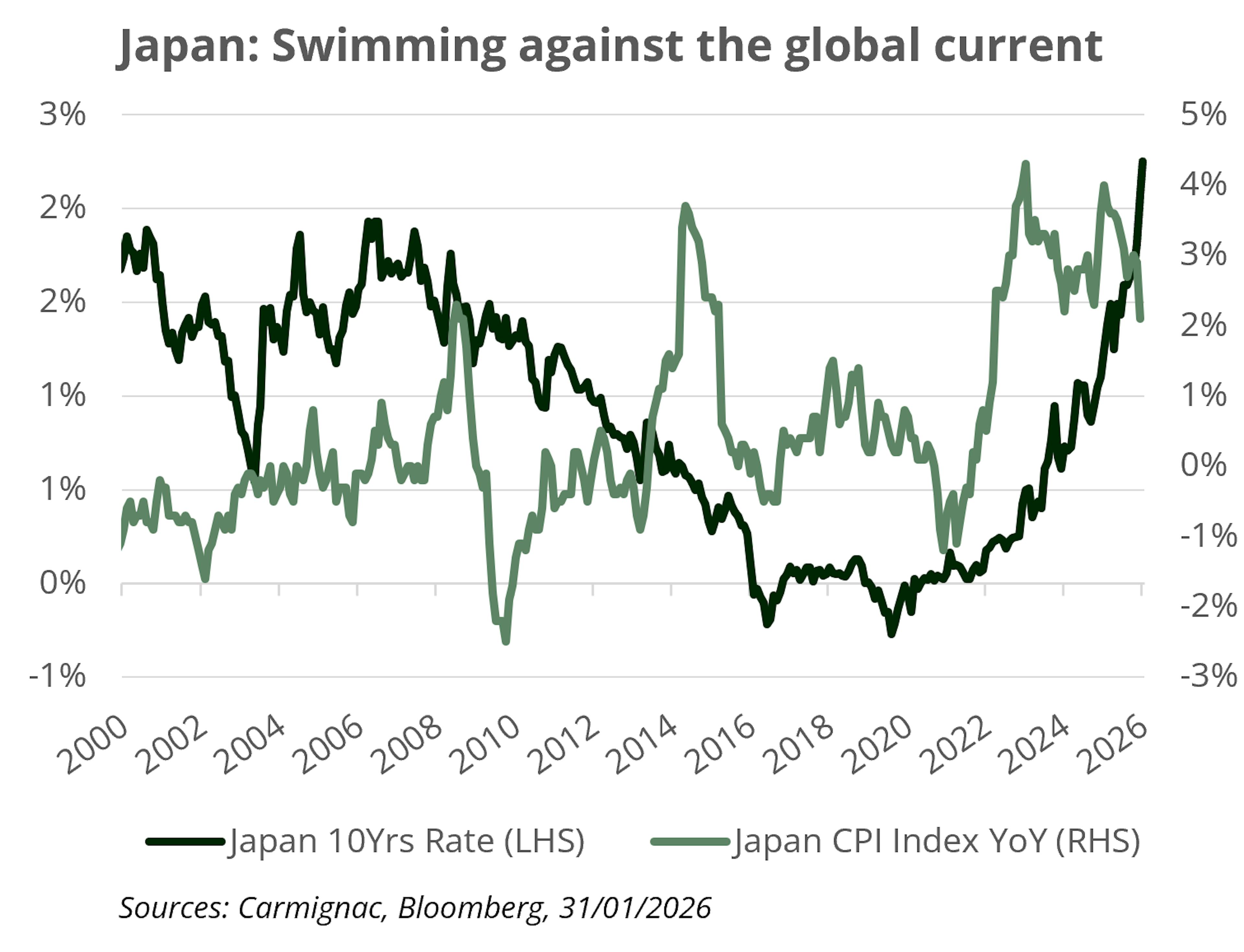

Japan: From deflationary outlier to repricing risk

For more than three decades, Japan defied gravity. Growth was subdued, inflation absent, and government bond yields hovered near zero, even as public debt climbed to levels unmatched in the developed world. That equilibrium, sustained by financial repression, central bank dominance and vast external asset accumulation, is now shifting. Inflation has re-emerged, wage negotiations are delivering the strongest increases in a generation, and nominal GDP is regaining momentum. What once appeared cyclical, increasingly looks structural: corporate pricing behaviour is evolving, labour shortages are binding in a rapidly ageing society, and inflation expectations are adjusting. In a country where almost 30% of the population is over 654, we believe labour scarcity is structural rather than temporary.

The decisive election of Sanae Takaichi reinforces this inflection point. With a strong mandate, the new administration is advancing industrial policy, energy security and defence initiatives, alongside a rapid €117 billion stimulus package5 and targeted tax relief aimed at cushioning households from persistent food inflation. Fiscal activism is no longer merely counter-cyclical support; it has become strategic. While Japan retains fiscal capacity—supported by its position as the world’s largest net external creditor — the macro-financial regime is changing.

For bond markets, the implications are significant. The debt burden itself is not new, but the environment in which it is financed has changed. Inflation expectations are no longer anchored at zero and, even if headline pressures moderate, greater volatility argues for a rebuilding of the term premium. As the BoJ gradually retreats and private investors absorb more issuance, compensation for duration and inflation risk should rise. Normalisation is cautious but deliberate: yield curve control has been diluted, and policy rates have turned positive.

While policymakers remain mindful of financial stability — aware that abrupt moves could unsettle global carry trades — they cannot allow inflation expectations to drift. Further measured tightening therefore remains the most credible course.

The adjustment is unlikely to be uniform across the curve. Upward pressure should remain concentrated in intermediate maturities, while the long end may stabilise after its recent repricing. Thirty-year yields have returned to positive real territory, a level that could attract more durable demand. In an economy rediscovering nominal growth, permanently repressed yields are no longer the only plausible anchor.

Inflation: The market’s blind spot

Another of our core convictions is that the global economy is shifting towards a regime of structurally higher inflation. The powerful disinflationary forces of the past three decades — globalisation, abundant labour, cheap energy, and fiscal restraint — are giving way to a costlier model built on ecological transition, nearshoring, national security, and persistent fiscal activism.

Nowhere is this transition more visible than in the US. The economy continues to operate close to or above potential, supported by AI-driven capital expenditure and sustained fiscal expansion. Beyond its productivity promise, the AI investment cycle is capital- and resource-intensive: data centre build-outs, rising energy demand and strategic commodity inputs are already generating pockets of price pressure. Nominal growth remains firm and the output gap positive, conditions under which inflation rarely returns smoothly to target.

Recent data confirm this stickiness. Core inflation has reaccelerated, particularly in services, where wage-intensive and inertial components remain inconsistent with a durable 2% regime6. Measures of underlying momentum — including supercore readings and the breadth of components running above target — suggest that price pressures remain more diffused than headline trends imply. Shelter disinflation is proving slower and more uneven than expected, while tariff-related pressures continue to feed through as inventories are rebuilt at higher import costs.

Policy dynamics add further complexity. While the Fed has adopted a more dovish stance and markets price additional easing, fiscal policy remains expansionary and growth resilient. At the same time, restrictive immigration policies are constraining labour supply just as demand strengthens, raising the risk of renewed wage pressures. Markets continue to anchor long-term inflation expectations of near 2%, a positioning that appears complacent relative to underlying macro dynamics.

Geopolitical risks reinforce this asymmetry. Recent US–Israel military action against Iran and disruptions to tanker traffic through the Strait of Hormuz have pushed crude prices higher, reminding investors how quickly energy shocks can interrupt disinflation and reintroduce upside risks to headline inflation.

We are not predicting a renewed inflation shock. Rather, inflation is likely to settle on a higher-for-longer plateau in an environment where growth remains resilient and supply constraints linger. We therefore express this conviction through exposure to US breakeven inflation strategies, which we view both as an efficient way to capture the asymmetry in inflation risks and as a portfolio hedge against a macro regime in which price pressures prove more persistent than currently discounted.

Emerging markets: Discipline rewarded

Emerging market local debt entered 2026 with a rare alignment of supportive forces. US exceptionalism is fading, global growth is moderating, and inflation across many emerging economies continues to ease, creating room for more accommodative monetary policy. Real yields remain attractive, debt dynamics are generally more favourable than in developed markets, and volatility has structurally declined.

In an environment shaped by a weaker USD and expected Fed easing, local rate markets are well positioned to deliver both carry and duration gains.

That constructive backdrop, however, does not apply uniformly across the universe. Selectivity is essential. We are focusing on countries where restrictive policy settings, improving fundamentals and credible central banks create clear room for rates to decline.

In Eastern Europe, Hungary stands out. Inflation is firmly on a disinflation path, real yields remain high, and policy rates are still restrictive. At the same time, the current account has improved markedly, and wage pressures have moderated, strengthening the macro backdrop and allowing scope for gradual rate normalisation7. The Czech Republic similarly combines easing inflation with disciplined policymaking and room for further cuts.

In Latin America, Brazil and Mexico offer compelling opportunities. Brazil’s Selic rate remains elevated in the mid-teens8, providing substantial carry, while inflation is moderating and growth is slowing, paving the way for eventual easing. Mexico also combines high real rates with a central bank already in a cutting cycle.

Across these markets, we see an attractive balance between income generation and potential capital appreciation — a combination increasingly scarce in developed fixed income markets.

1Congressional Budget Office (CBO) fiscal outlook, February 2026. The Budget and Economic Outlook: 2026 to 2036 | Congressional Budget Office.

2ECB press conference, 5 February 2026. PRESS CONFERENCE.

3French government bonds.

4Statistics Bureau Home Page/Population Estimates/Current Population Estimates as of October 1, 2024.

5Press Conference by Prime Minister TAKAICHI Sanae regarding Comprehensive Economic Measures and Other Matters (Speeches and Statements by the Prime Minister) | Prime Minister's Office of Japan.

6U.S. Bureau of labor statistics, February 2026. Consumer Price Index Summary - 2026 M01 Results.

7Hungarian central statistical office.

8Banco Central do Brasil. Selic interest rate.

The Carmignac fixed income range

Carmignac Portfolio Sécurité FW EUR Acc

- Recommended minimum investment horizon

- 2 years

- Risk indicator*

- 2/7

- SFDR - Fund Classification**

- Article 8

*Risk Scale from the KID (Key Information Document). Risk 1 does not mean a risk-free investment. This indicator may change over time. **Sustainable Finance Disclosure Regulation (SFDR) 2019/2088. The SFDR classification of the Funds may change over time.

Main risks of the fund

Carmignac Portfolio Flexible Bond A EUR Acc

- Recommended minimum investment horizon

- 3 years

- Risk indicator*

- 2/7

- SFDR - Fund Classification**

- Article 8

*Risk Scale from the KID (Key Information Document). Risk 1 does not mean a risk-free investment. This indicator may change over time. **Sustainable Finance Disclosure Regulation (SFDR) 2019/2088. The SFDR classification of the Funds may change over time.

Main risks of the fund

Carmignac Sécurité AW EUR Acc

- Recommended minimum investment horizon

- 2 years

- Risk indicator*

- 2/7

- SFDR - Fund Classification**

- Article 8

*Risk Scale from the KID (Key Information Document). Risk 1 does not mean a risk-free investment. This indicator may change over time. **Sustainable Finance Disclosure Regulation (SFDR) 2019/2088. The SFDR classification of the Funds may change over time.

Main risks of the fund

Carmignac Portfolio Global Bond A EUR Acc

- Recommended minimum investment horizon

- 3 years

- Risk indicator*

- 2/7

- SFDR - Fund Classification**

- Article 8

*Risk Scale from the KID (Key Information Document). Risk 1 does not mean a risk-free investment. This indicator may change over time. **Sustainable Finance Disclosure Regulation (SFDR) 2019/2088. The SFDR classification of the Funds may change over time.

Main risks of the fund

Carmignac Portfolio EM Debt A EUR Acc

- Recommended minimum investment horizon

- 3 years

- Risk indicator*

- 3/7

- SFDR - Fund Classification**

- Article 8

*Risk Scale from the KID (Key Information Document). Risk 1 does not mean a risk-free investment. This indicator may change over time. **Sustainable Finance Disclosure Regulation (SFDR) 2019/2088. The SFDR classification of the Funds may change over time.

Main risks of the fund

MARKETING COMMUNICATION. Please refer to the KID/KIID/prospectus of the Fund before making any final investment decisions. This document is intended for professional clients.

This document may not be reproduced, in whole or in part, without prior authorisation from the management company. It does not constitute a subscription offer, nor does it constitute investment advice. The information contained in this document may be partial information and may be modified without prior notice. The Management Company can cease promotion in your country anytime. Investors have access to a summary of their rights in French, English, German, Dutch, Spanish, Italian at the following link (paragraph 5 “Summary of investor rights”): https://www.carmignac.com/en/regulatory-information. The decision to invest in the promoted fund should take into account all its characteristics or objectives as described in its prospectus. The Funds are common funds in contractual form (FCP) conforming to the UCITS Directive under French law. Carmignac Portfolio refers to the sub-funds of Carmignac Portfolio SICAV, an investment company under Luxembourg law, conforming to the UCITS Directive. The reference to a ranking or prize, is no guarantee of the future results of the UCITS or the manager. Past performance is not necessarily indicative of future performance. Performances are net of fees (excluding possible entrance fees charged by the distributor). The return may increase or decrease as a result of currency fluctuations, for the shares which are not currency-hedged. Reference to certain securities and financial instruments is for illustrative purposes to highlight stocks that are or have been included in the portfolios of funds in the Carmignac range. This is not intended to promote direct investment in those instruments, nor does it constitute investment advice. The Management Company is not subject to prohibition on trading in these instruments prior to issuing any communication. The portfolios of Carmignac funds may change without previous notice. Access to the Funds may be subject to restrictions with regard to certain persons or countries. The Funds may not be offered or sold, directly or indirectly, for the benefit or on behalf of a U.S. person, according to the definition of the US Regulation S and/or FATCA. The Funds present a risk of loss of capital. The risk, fees and ongoing charges are described in the KIDs/KIIDs (Key Information Document/Key Investor Information Document). The Funds' respective prospectuses, KIDs/KIIDs, NAV and annual reports are available at www.carmignac.com, or upon request to the Management Company. The KIDs/KIIDs must be made available to the subscriber prior to subscription.

- Portugal: The Funds are registered with the Comissão do Mercado de Valores (CMVM). The Funds’ respective prospectuses, KIDs and annual reports are available at www.carmignac.com/pt-pt. The KIDs must be made available to the subscriber prior to subscription.

- In Switzerland, the Funds’ respective prospectuses, KIDs and annual reports are available at www.carmignac.com/en-ch or through our representative in Switzerland, CACEIS (Switzerland), S.A., Route de Signy 35, CH-1260 Nyon. The paying agent is CACEIS Bank, Montrouge, succursale de Nyon / Suisse, Route de Signy 35, 1260 Nyon. The KIDs must be made available to the subscriber prior to subscription.

- In the United Kingdom: the Funds’ respective prospectuses, KIIDs and annual reports are available at www.carmignac.com/en-gb, or upon request to the Management Company, or for the French Funds, at the offices of the facilities Agent, Carmignac UK Ltd, 2 Carlton House Terrace, London, SW1Y 5AF. This document was prepared by Carmignac Gestion, Carmignac Gestion Luxembourg or Carmignac UK Ltd. FP Carmignac ICVC (the “Company”) is an Investment Company with variable capital incorporated in England and Wales under registered number 839620 and is authorised by the FCA with effect from 4 April 2019 and launched on 15 May 2019. FundRock Partners Limited is the Authorised Corporate Director (the “ACD”) of the Company and is authorised and regulated by the FCA. Registered Office: Hamilton Centre, Rodney Way, Chelmsford, Essex, CM1 3BY, UK; Registered in England and Wales with number 4162989. Carmignac Gestion Luxembourg SA has been appointed as the Investment Manager and distributor in respect of the Company. Carmignac UK Ltd (Registered in England and Wales with number 14162894) has been appointed as a sub-Investment Manager of the Company and is authorised and regulated by the Financial Conduct Authority with FRN:984288.

- In Belgium: This document has not been submitted to FSMA for validation. It is intended for professionals only. This communication is published by Carmignac Gestion S.A., a portfolio management company approved by the Autorité des Marchés Financiers (AMF) in France, and its Luxembourg subsidiary Carmignac Gestion Luxembourg, S.A., an investment fund management company approved by the Commission de Surveillance du Secteur Financier (CSSF). “Carmignac” is a registered trademark. “Investing in your Interest” is a slogan associated with the Carmignac trademark. This document does not constitute advice on any investment or arbitrage of transferable securities or any other asset management or investment product or service. The information and opinions contained in this document do not take into account investors’ specific individual circumstances and must never be interpreted as legal, tax or investment advice. The risks and fees are described in the KIDs (Key Information Documents). The prospectuses, KIDs, the net asset-values and the latest (semi-) annual management reports may be obtained, free of charge, in French or in Dutch, from the management company (tel. +352 46 70 60 1) or by consulting its website or www.fundinfo.com. These materials may also be obtained from Caceis Belgium S.A., the financial service provider in Belgium, at the following address: avenue du port, 86c b320, B-1000 Brussels. In case of subscription to a fund subject to Article 19bis of the Belgian Income Tax Code (CIR92), the investor will have to pay, upon redemption of his or her shares, a withholding tax of 30% on the income (in the form of interest, or capital gains or losses) derived from the return on assets invested in debt claims. Distributions are subject to withholding tax of 30% without income distinction. In case of subscription in a French investment fund (fonds commun de placement or FCP), you must declare on tax form, each year, the share of the dividends (and interest, if applicable) received by the Fund. Any complaint may be referred to complaints@carmignac.com or CARMIGNAC GESTION - Compliance and Internal Controls - 24 place Vendôme Paris France or on the website www.ombudsfin.be.

CARMIGNAC GESTION - 24, place Vendôme - F-75001 Paris - Tél : (+33) 01 42 86 53 35. Investment management company approved by the AMF -Public limited company with share capital of € 13,500,000 - RCS Paris B 349 501 676.

CARMIGNAC GESTION Luxembourg - City Link - 7, rue de la Chapelle - L-1325 Luxembourg - Tel : (+352) 46 70 60 1. Subsidiary of Carmignac Gestion. Investment fund management company approved by the CSSF. Public limited company with share capital of € 23,000,000 - RCS Luxembourg B 67 549.