![[Main Media] [Funds Focus] Bridge](https://carmignac.imgix.net/uploads/NextImage/0001/02/26ad7f7eb70cc9f1137127c5b230d8042189f9e1.jpeg?auto=format%2Ccompress&crop=faces&fit=crop&w=3840)

Carmignac Absolute Return Europe: Letter from the Fund Managers

Dear Investors,

The fourth quarter was the first full quarter as new managers of the Carmignac Absolute Return Europe fund. During the last quarter, the return of the Fund (A share class) was +2.44%, while for the calendar year the fund registered a performance of +0.01%.

The last quarter of the year proved to be a period of extreme volatility for capital markets across all asset classes driven largely by macro factors, most notably central bank policy communication and inflation data. An acceleration of the selling pressure which began in July saw October produce the worst market performance of the year. This was led by a toxic combination of bond yields temporarily bursting through 5%, a level not hit since 2007, weakening macro data in Europe and a rise in geopolitical tension in the Middle East. As we moved into November, the picture began to change, as the inflation data began to show a material decline. This decline was significant enough to catalyze a drop in the US 10-year yield by 65bps, which was the largest one day drop since 2008. This led investors to believe that the Federal Reserve (Fed) and other central banks were done on rate rises and what followed was a significant tightening of credit spreads and a highly rotational rally in equities, driven by aggressive short covering. The rally continued through December, as inflation data continued to surprise to the downside driving bond yields down below 4%, effectively to where they were in February and pushing equity prices higher.

Q4 was the first full quarter for us as new managers of the Fund and we are pleased to be able to report 3 consecutive months of positive returns in what have been incredibly volatile and challenging market conditions. In October, we produced a positive return of +94 bps during the sell-off with a very positive contribution from our short book and portfolio hedging. In November, with an improving inflation picture we had to make significant changes to the portfolio, covering shorts and adding longs in names that we thought would benefit from lower rates and improving market sentiment which saw us move from flat/slightly short to a net long position. This was achieved by adding exposure to Industrials, Technology, Real Estate and Construction. December saw a continuing pattern with equity markets continuing to rally to new highs, following the pivot from the Fed indicating that the rate tightening cycle was over and that the next policy move would be cuts.

Looking into the portfolio, the largest positive portfolio contributions for the quarter came from Industrials, Technology, Communications Services and Materials. All sectors in our portfolio produced a positive return over the quarter with the exception of Healthcare, which was a small laggard. At the stock level, our largest winners and losers were:

Winners - a combination of longs and shorts

- Microsoft Long - positive numbers and a key beneficiary of the Artificial Intelligence (AI) theme.

- ASML Long - beneficiary of reshoring the semiconductor industry.

- Meta Long - improving top line growth and margins.

- French capital goods short - significant profits warning.

- German healthcare service provider short - potential negative impact of GLP-1 drugs.

Losers - mainly shorts impacted by short covering rally

- Swiss semiconductor equipment short - improving sentiment despite stratospheric valuation.

- Swiss MedTech - short covering.

- Consumer tech short - rallied despite disappointing numbers.

- Dutch MedTech short - short covering.

- Prada - negative sentiment on luxury / Chinese consumer spending.

Markets have now run very hard into year end and are now pricing in a Goldilocks scenario of significant rate cuts for 2024 alongside a soft landing. This is driven by anticipation of a further fall in inflation, ongoing relatively full employment, and no recession.

While it is highly likely that there will be interest rate cuts in 2024, we suspect that too much optimism is priced in too soon. Therefore, in the short term, we believe there is a possibility of some disappointment regarding the timing of monetary easing and that the first rate cuts may occur in March or May. Meanwhile, the economic data is continuing to deteriorate as the impact of previous significant interest rate increases is finally beginning to feed through into the economy. Even the highly resilient US economy is seeing softness in industrial activity with new order data in decline. Similarly, European data is suggesting we could be heading back to a period of no growth and potentially outright deflation.

Even if a new cycle of interest rate cuts should support an economic recovery during 2024, the positive effects may not become apparent until the second half of the year and the degree of interest rate cuts will be determined by the pace of economic slowdown, which is a risk to the earnings outlook, therefore it is important to be mindful of why rates will eventually be cut. If they are solely driven by a decline in inflation expectations while economic growth expectations remain steady, then clearly the markets will welcome that and at worst, the risk might be for some short-term consolidation after a strong 2023 year end run. However, if rate cuts come due to further deteriorating economic data, weaker corporate earnings outlook, the risk for markets is skewed to the downside, particularly in the short term, in our opinion.

Currently the data is mixed, economic indicators are weak, but so far corporate earnings have held up reasonably well. Therefore, we believe that corporate FY23 earnings announcements with 2024 outlook commentary will be a catalyst for markets and how individual stocks will trade in coming weeks/months. As such, in the short term we are inclined to tactically reduce our net exposures by locking in some of recent single stock gains from the November-December rally and add back to our single short book. Also, in early January, we will attend a couple of corporate conferences, where we will get the chance to meet with several European corporates which should help us form a stronger view around themes and individual stock positions.

For the year as a whole, 2024 should emerge to be a more ‘normal’ year. After 2-3 years of the world being impacted by covid, wars & unprecedented central bank and government interventions, all of which collectively caused so many industries falling out of sync with their normal cycles (supply chain disruptions, inventory corrections etc.), finally in 2024, cycles should again begin to align themselves to more historical patterns. This should be a good thing as it should add visibility, not only for how corporates can manage their own businesses, but also for us as investors. Having said that, we must recognize that 2024 could still be a year of further turbulence brought about by fluctuating economic fundamentals, pace of rate cuts, as well as heightened geopolitical risk due to increasing armed conflicts and many elections in a significant proportion of the world, either of which could lead to shifts in government policies.

Notwithstanding some of the short-term risks and the various challenges for 2024, we are very optimistic about the prospects for an Equity Long/short strategy like ours for the year ahead. Investors and asset allocators have now had to endure a long period of extreme uncertainty and volatility all caused by extreme events (Covid & Wars) and subsequent unprecedented central bank interventions. These events have caused considerable imbalances for financial markets, catalyzing significant flows between asset classes, which from hereon should normalize. Therefore, if rates have now peaked and will trend lower, it should be very supportive to equities again as an asset class and once the prospect and path to economic recovery emerges, spurred on by structural trends such as onshoring, de-globalization, AI and much else, it should make for a rich stock picking environment.

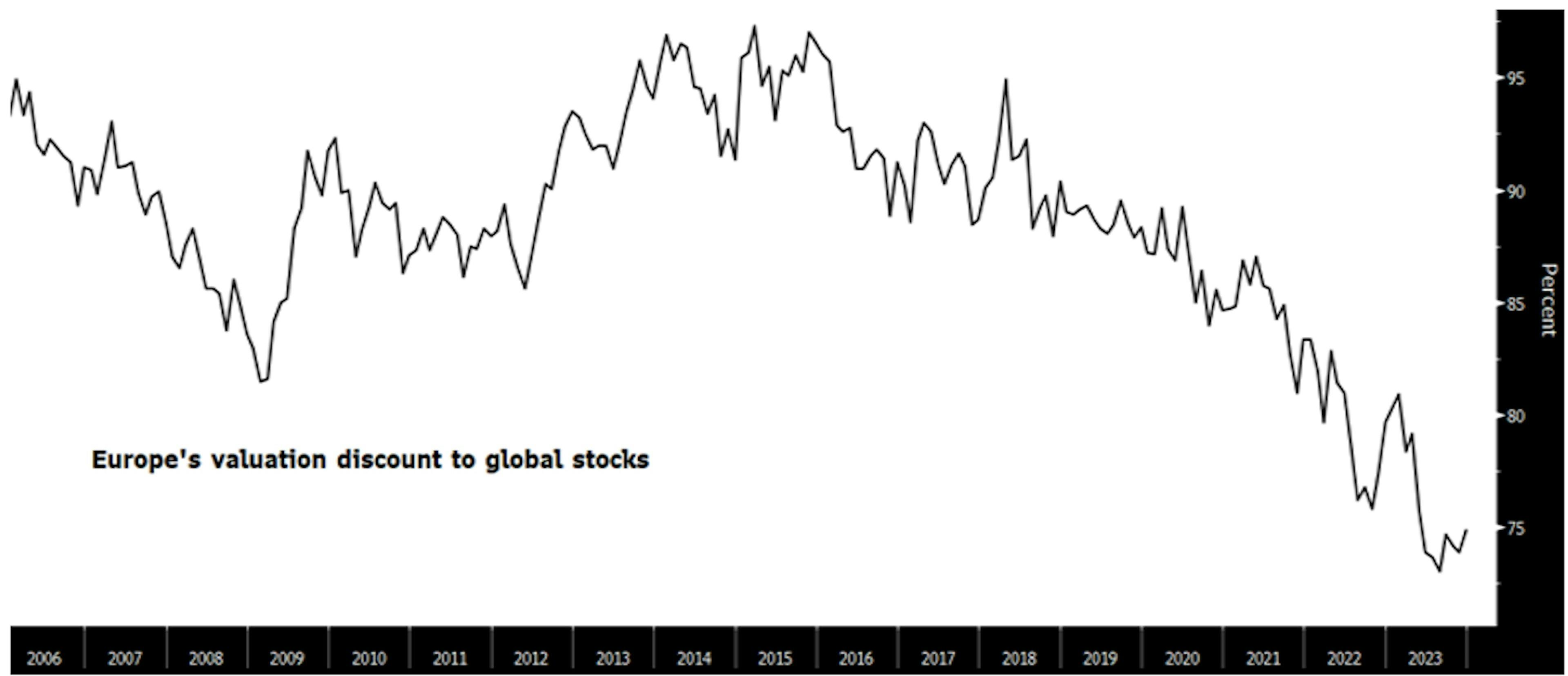

We believe that many of the structural trends within Technology (AI) & Healthcare (GLP1) will continue to dominate and these are areas we will continue to like and seek exposure to. But at the same time, we believe there are several very interesting trends and value opportunities to emerge in Europe. Whilst European equities have often traded at a discount to other Equity markets, just as they do yet again post the crisis (UK domestic equities in particular), with lower rates and eventually a recovery on the horizon, there should be plenty of opportunities. Therefore, once we have a clearer understanding of the economic backdrop and the short-term corporate earnings, we believe Europe offers an attractive starting point, with tons of potential for recovery.

Finally, we think it is important to remind our investors that as our investment strategy has no strong style biases and a truly opportunistic approach to how we invest, we are now coming out of these years dominated by some version of a crisis and we can be fully flexible to capture any new trends and opportunities emerging. We aim to deliver a steady and compounding return at relatively low volatility. This is our promise to our investors. Having just completed our first full quarter managing these funds at Carmignac and delivering returns in line with our targeted risk level, we are extremely confident in our ability to deliver for our investors in 2024 and the years ahead.

EU valuations discount to Global stocks.

Carmignac Absolute Return Europe

Carmignac Absolute Return Europe A EUR Acc

- Recommended minimum investment horizon

- 3 years

- Risk indicator*

- 3/7

- SFDR - Fund Classification**

- Article 8

*Risk Scale from the KID (Key Information Document). Risk 1 does not mean a risk-free investment. This indicator may change over time. **Sustainable Finance Disclosure Regulation (SFDR) 2019/2088. The SFDR classification of the Funds may change over time.

Main risks of the fund

Fees

- Entry costs

- 4.00% of the amount you pay in when entering this investment. This is the most you will be charged. Carmignac Gestion doesn't charge any entry fee. The person selling you the product will inform you of the actual charge.

- Exit costs

- We do not charge an exit fee for this product.

- Management fees and other administrative or operating costs

- 2.15% of the value of your investment per year. This estimate is based on actual costs over the past year.

- Performance fees

- 20.00% max. of the outperformance if the performance is positive and the net asset value exceeds the high-water mark. The actual amount will vary depending on how well your investment performs. The aggregated cost estimation above includes the average over the last 5 years, or since the product creation if it is less than 5 years.

- Transaction Cost

- 1.05% of the value of your investment per year. This is an estimate of the costs incurred when we buy and sell the investments underlying the product. The actual amount varies depending on the quantity we buy and sell.

Performance

| Carmignac Absolute Return Europe | 14.6 | 4.4 | -1.3 | 5.2 | 12.6 | -6.4 | 0.0 | 3.6 | -0.6 | 1.7 |

| Carmignac Absolute Return Europe | + 2.2 % | + 1.8 % | + 4.4 % |

Source: Carmignac at Feb 27, 2026.

Past performance is not necessarily indicative of future performance. Performances are net of fees (excluding possible entrance fees charged by the distributor). The Fund presents a risk of loss of capital.

Reference Indicator: -

Marketing communication. Please refer to the KID/KIID, prospectus of the fund before making any final investment decisions. This document is intended for professional clients.

This material may not be reproduced, in whole or in part, without prior authorisation from the Management Company. This material does not constitute a subscription offer, nor does it constitute investment advice. This material is not intended to provide, and should not be relied on for, accounting, legal or tax advice. This material has been provided to you for informational purposes only and may not be relied upon by you in evaluating the merits of investing in any securities or interests referred to herein or for any other purposes. The information contained in this material may be partial information and may be modified without prior notice. They are expressed as of the date of writing and are derived from proprietary and non-proprietary sources deemed by Carmignac to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by Carmignac, its officers, employees or agents.

Past performance is not necessarily indicative of future performance. Performances are net of fees (excluding possible entrance fees charged by the distributor). The return may increase or decrease as a result of currency fluctuations, for the shares which are not currency-hedged.

Reference to certain securities and financial instruments is for illustrative purposes to highlight stocks that are or have been included in the portfolios of funds in the Carmignac range. This is not intended to promote direct investment in those instruments, nor does it constitute investment advice. The Management Company is not subject to prohibition on trading in these instruments prior to issuing any communication. The portfolios of Carmignac funds may change without previous notice. The reference to a ranking or prize, is no guarantee of the future results of the UCIS or the manager.

Morningstar Rating™ : © Morningstar, Inc. All Rights Reserved. The information contained herein: is proprietary to Morningstar and/or its content providers; may not be copied or distributed; and is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information.

Access to the Funds may be subject to restrictions regarding certain persons or countries. This material is not directed to any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the material or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not access this material. Taxation depends on the situation of the individual. The Funds are not registered for retail distribution in Asia, in Japan, in North America, nor are they registered in South America. Carmignac Funds are registered in Singapore as restricted foreign scheme (for professional clients only). The Funds have not been registered under the US Securities Act of 1933. The Funds may not be offered or sold, directly or indirectly, for the benefit or on behalf of a «U.S. person», according to the definition of the US Regulation S and FATCA.

The risks, fees and ongoing charges are described in the KID (Key Information Document). The KID must be made available to the subscriber prior to subscription. The subscriber must read the KID. Investors may lose some or all their capital, as the capital in the funds are not guaranteed. The Funds present a risk of loss of capital.

The Funds’ prospectus, KIDs, NAVs and annual reports are available at www.carmignac.com/en, or upon request to the Management Carmignac Portfolio refers to the sub-funds of Carmignac Portfolio SICAV, an investment company under Luxembourg law, conforming to the UCITS Directive. The French investment funds (fonds communs de placement or FCP) are common funds in contractual form conforming to the UCITS or AIFM Directive under French law.

In the United Kingdom: the Funds’ respective prospectuses, KIIDs and annual reports are available at www.carmignac.com/en-gb, or upon request to the Management Company, or for the French Funds, at the offices of the acilities Agent, Carmignac UK Ltd, 2 Carlton House Terrace, London, SW1Y 5AF. This document was prepared by Carmignac Gestion, Carmignac Gestion Luxembourg or Carmignac UK Ltd. FP Carmignac ICVC (the “Company”) is an Investment Company with variable capital incorporated in England and Wales under registered number 839620 and is authorised by the FCA with effect from 4 April 2019 and launched on 15 May 2019. FundRock Partners Limited is the Authorised Corporate Director (the “ACD”) of the Company and is authorised and regulated by the FCA. Registered Office: Hamilton Centre, Rodney Way, Chelmsford, Essex, CM1 3BY, UK; Registered in England and Wales with number 4162989. Carmignac Gestion Luxembourg SA has been appointed as the Investment Manager and distributor in respect of the Company. Carmignac UK Ltd (Registered in England and Wales with number 14162894) has been appointed as a sub-Investment Manager of the Company and is authorised and regulated by the Financial Conduct Authority with FRN:984288.

In Switzerland: the prospectus, KIDs and annual report are available at www.carmignac.com/en-ch, or through our representative in Switzerland, CACEIS (Switzerland), S.A., Route de Signy 35, CH-1260 Nyon. The paying agent is CACEIS Bank, Montrouge, Nyon Branch / Switzerland, Route de Signy 35, 1260 Nyon.

In Belgium: This document is intended for professional clients. This content has not been validated by FSMA. The decision to invest in the promoted fund should take into account all its characteristics or objectives as described in its prospectus. This communication is published by Carmignac Gestion S.A., a portfolio management company approved by the Autorité des Marchés Financiers (AMF) in France, and its Luxembourg subsidiary Carmignac Gestion Luxembourg, S.A., an investment fund management company approved by the Commission de Surveillance du Secteur Financier (CSSF). “Carmignac” is a registered trademark. “Investing in your Interest” is a slogan associated with the Carmignac trademark. This document does not constitute advice on any investment or arbitrage of transferable securities or any other asset management or investment product or service. The information and opinions contained in this document do not take into account investors’ specific individual circumstances and must never be interpreted as legal, tax or investment advice. The information contained in this document may be partial and could be changed without notice. This document may not be reproduced in whole or in part without prior authorisation. The risks and fees are described in the KID (Key Information Document). The prospectus, KID, the net asset-values and the latest (semi-) annual management report may be obtained, free of charge, in French or in Dutch, from the management company (tel. +352 46 70 60 1) or by consulting its website or www.fundinfo.com. These materials may also be obtained from Caceis Belgium S.A., the financial service provider in Belgium, at the following address: avenue du port, 86c b320, B-1000 Brussels. The Fund (fonds commun de placement or FCP) is a common fund in contractual form conforming to the UCITS Directive under French law. Access to the Fund may be subject to restrictions regarding certain persons or countries. The Funds are not registered for retail distribution in Asia, in Japan, in North America, nor are they registered in South America. Carmignac Funds are registered in Singapore as restricted foreign scheme (for professional clients only). The Funds have not been registered under the US Securities Act of 1933. The Funds may not be offered or sold, directly or indirectly, for the benefit or on behalf of a «U.S. person», according to the definition of the US Regulation S and FATCA. In case of subscription to a fund subject to Article 19bis of the Belgian Income Tax Code (CIR92), the investor will have to pay, upon redemption of his or her shares, a withholding tax of 30% on the income (in the form of interest, or capital gains or losses) derived from the return on assets invested in debt claims. Distributions are subject to withholding tax of 30% without income distinction. In case of subscription in a French investment fund (fonds commun de placement or FCP), you must declare on tax form, each year, the share of the dividends (and interest, if applicable) received by the Fund. Any complaint may be referred to complaints@carmignac.com or CARMIGNAC GESTION - Compliance and Internal Controls - 24 place Vendôme Paris France or on the website www.ombudsfin.be.

The Management Company can cease promotion in your country anytime. Investors have access to a summary of their rights at section 5 entitled "summary of investor rights" on the following links: UK ; Switzerland ; France ; Luxembourg ; Sweden. Belgium (French) ; Belgium (Dutch)

For Carmignac Portfolio Long-Short European Equities: Carmignac Gestion Luxembourg SA in its capacity as the Management Company for Carmignac Portfolio, has delegated the investment management of this Sub-Fund to White Creek Capital LLP (Registered in England and Wales with number OCC447169) from 2nd May 2024. White Creek Capital LLP is authorised and regulated by the Financial Conduct Authority with FRN : 998349.

Carmignac Private Evergreen refers to the Private Evergreen sub-fund of the SICAV Carmignac S.A. SICAV – PART II UCI, registered with the Luxembourg RCS under number B285278.