Emerging Market Debt: Resilience in a more volatile world

- Emerging markets entered 2026 from a position of strength, with higher real rates, stronger external balances and more credible policy frameworks.

- While the March oil shock triggered significant volatility, the absence of broader financial stress highlighted the resilience of EM debt relative to previous crisis episodes.

- The asset class continues to benefit from improving fundamentals across many EM countries, supported by attractive carry, lower US real yields and a softer dollar.

- Positioning remains constructive but selective: we favour high-yield sovereign credit and selected FX opportunities supported by carry and improving fundamentals, while remaining more cautious on local rates as elevated oil prices and inflation pressures could trigger hiking cycles in some countries.

Emerging markets (EM) entered 2026 from a position of strength. The March oil shock disrupted the market narrative, but not the underlying cycle. While the initial reaction was sharp, the absence of broader market dislocations, resilient credit markets and the rebound in April all pointed to a repricing rather than a regime shift, reinforcing our constructive view on EM fixed income.

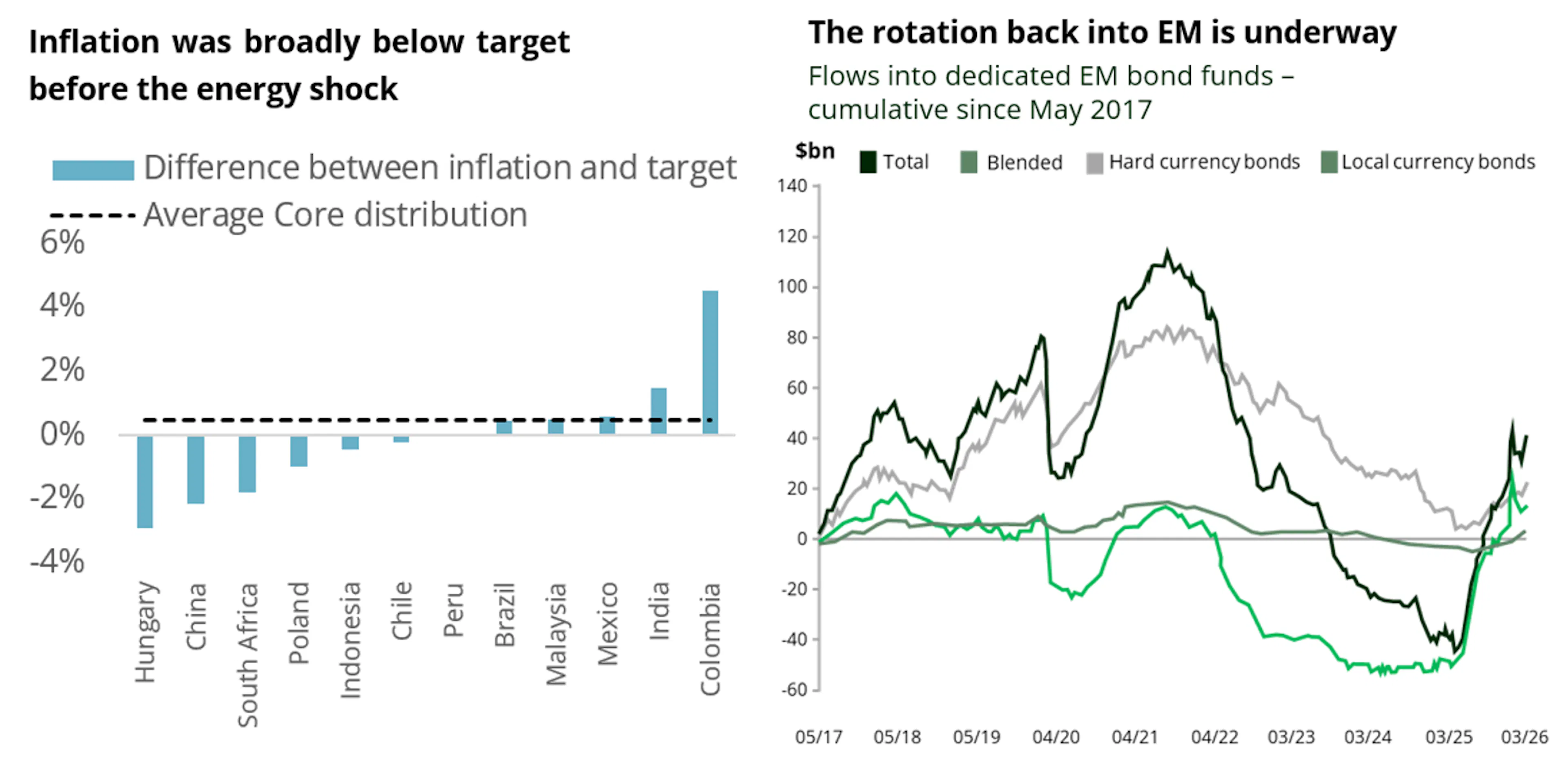

EM debt has undergone a significant adjustment since the post-Covid inflation shock, the aftershocks of Russia’s invasion of Ukraine and more recent geopolitical episodes such as ‘Liberation Day’. Rates reset higher, currencies cheapened, investor positioning was reduced and policymakers rebuilt credibility.

As a result, EM now enters this phase with stronger carry, healthier external balances, rebuilt reserve buffers and more orthodox central banks than in previous energy-shock episodes. This stronger starting point helps explain why the recent surge in oil prices generated volatility, but not broader financial stress.

From disinflation to central bank reaction

The year began in a supportive environment, with a softer dollar, easing US real yields and still-light investor positioning. This combination supported both FX and local markets, while hard-currency debt benefited from carry and improving credit fundamentals.

This benign backdrop was abruptly interrupted by the escalation in the Middle East. The market reaction followed a familiar pattern: local curves sold off sharply, front-end pricing shifted from rate cuts toward renewed tightening expectations, and oil-importing currencies underperformed. Local debt led the move, as the narrative shifted rapidly from disinflation to energy-driven inflation risk. March proved challenging, with EM hard-currency debt posting its weakest monthly performance since 2022, while local markets experienced their largest drawdown since the Covid shock.

The shock also revealed clear dispersion across the asset class. Performance diverged along macro fundamentals: oil exporters outperformed importers, high real-rate markets proved more resilient, and regional differences widened. LatAm and CEEMEA1 held up better than Asia, supported by higher carry, stronger terms of trade and, in many cases, more credible policy frameworks, while Asia lagged given lower carry and greater sensitivity to the energy shock.

More importantly, we believe what did not happen is more telling. There was no generalized loss of market access, no balance-of-payments stress and no indiscriminate sell-off across EM FX or credit. Compared with previous energy shocks, the adjustment remained contained.

April confirmed this resilience. As geopolitical tensions partially eased, EM assets rebounded strongly, with credit retracing most of its widening and local markets recovering as extreme tightening scenarios were priced out, leaving EM among the best-performing segments of global fixed income year-to-date as indicated below.

Beyond the shock: why the cycle remains intact

Our central scenario is not a return to the pre-shock environment, but rather a regime shaped by an ongoing oil shock and elevated uncertainty. Markets are tentatively leaning toward de-escalation, with partial normalization of shipping flows and oil prices stabilizing at elevated levels. However, the persistence of the shock remains the key uncertainty, leaving the backdrop better described as an unstable equilibrium than a settled regime.

In this context, EM central banks are unlikely to embark on a broad-based tightening cycle. While inflation risks warrant close monitoring, particularly where energy pass-through is rapid, the recent repricing from rate cuts to outright hikes already appears demanding in many markets and selective and limited hiking cycles may still emerge. We believe that central banks are more likely to act tactically to anchor expectations, especially where real rates are low, currencies are vulnerable or the oil shock proves persistent. The implication is targeted tightening rather than a generalized policy response, with a pause remaining the dominant baseline.

This reflects a stronger starting point than in previous cycles. Real rates are materially higher, providing a built-in buffer against inflation shocks and reducing the need for defensive tightening. External balances have improved, FX reserves have been rebuilt and central banks have maintained credibility. Together, these factors provide policymakers with greater flexibility and reduce the need for mechanical reactions to external shocks.

The broader backdrop remains supportive. Lower US real yields and a softer dollar continue to underpin EM FX and local markets, while carry remains among the most attractive in global fixed income. In a more range-bound environment, this income cushion becomes the first line of defence.

Flows reinforce this view. After several years of outflows, investors remain structurally underweight EM. Should geopolitical conditions stabilize, capital can return quickly, particularly into liquid, high-carry segments.

Overall, the cycle remains intact, but the drivers of returns are evolving. Broad beta is giving way to greater selectivity, with increasing emphasis on carry, fundamentals and differentiation across countries.

Selective risk-taking in a more complex environment

As the cycle evolves and dispersion increases, selectivity becomes the key driver of returns. Through the shock, we kept hard-currency exposure broadly stable, reducing duration as volatility spiked, and rebuilding it as valuations improved. The portfolio now combines around 3.5 years of duration, a double-digit yield, a BBB- average rating and approximately 25% CDS/CDX protection, remaining invested but not complacent.

Sovereign credit: favouring carry, reform and asymmetry

In sovereign credit, we remain cautious on the most expensive segments, particularly low-carry investment-grade names where spreads offer limited room for error. By contrast, higher-yielding sovereigns continue to offer a more compelling combination of carry, valuation and upside potential, with risk premia that remain adequately compensated.

This leads us to focus on oil exporters, reform-driven stories and selected distressed or post-distressed situations where valuations still reflect outcomes significantly more adverse than our central scenario. This positioning remained broadly unchanged during the March shock. While higher oil prices increased volatility, they did not alter our preference for issuers with manageable external liquidity profiles and spreads already incorporating a degree of macro uncertainty.

Alongside selective exposures to Angola, Ecuador, Venezuela and Ukraine, we continue to favour Argentina and Côte d’Ivoire as differentiated expressions of reform and recovery.

Côte d’Ivoire – growth and stability at a discount

Côte d’Ivoire remains one of the most compelling high-yield stories. Growth is strong at 6–7% and increasingly diversified, supported by infrastructure investment and the development of new sectors. Recent hydrocarbon discoveries strengthen the medium-term external outlook, while IMF-backed policy management provides a credible anchor.

Yet eurobonds still offer yields above 8%, which appears inconsistent with a sovereign combining solid growth, moderate debt and improving external buffers. This disconnect reflects political risk premia rather than fundamental weakness, creating an attractive carry and compression opportunity.

Argentina – reform momentum meeting market reality

Argentina is transitioning from a post-restructuring recovery story to a more credible reform-driven credit. Fiscal adjustment has been front-loaded, delivering a rare primary surplus, while reserves are gradually rebuilding alongside a more orthodox policy mix and continued IMF engagement.

Despite being one of the most improved credits in EM over the past year, Argentina continues to trade wide relative to peers, leaving room for further spread compression as credibility builds and investor positioning, still light after years of outflows, normalises.

Beyond stabilisation, the external story reinforces the credit trajectory. Energy exports, led by Vaca Muerta, are scaling up rapidly and could turn the country into a structural net exporter, while mining continues to attract sustained FDI inflows. Together with a resilient agricultural base, this supports export growth, reserve accumulation and a stronger balance of payments.

FX: where carry, valuation and external adjustment meet

FX remains a key source of alpha in the current environment, and we have reduced dollar exposure in favour of selected EM currencies where carry, valuation and external dynamics offer the most compelling asymmetry, while the resilience of global growth despite recent volatility continues to support the broader EM FX backdrop.

Latin America remains a core area of conviction. The Brazilian real and the Mexican peso and continue to stand out among liquid EM currencies, offering attractive carry and operating in deep markets capable of absorbing renewed inflows. Both should benefit from a gradual normalization of geopolitical risk. In Brazil, elevated real rates and supportive terms of trade provide a meaningful buffer, while in Mexico, carry remains compelling and the broader macro framework helps limit downside risks despite higher energy prices.

Outside Latin America, positioning remains more selective. The Hungarian forint offers an attractive combination of high real rates, improving political dynamics and supportive medium-term prospects linked to closer European integration and the longer-term euro adoption theme. The offshore renminbi (CNH), by contrast, is less a carry story than a valuation one, supported by China’s persistent current account surplus and relatively strong external position.

Within Asia, our stance remains cautious. Lower carry, higher energy sensitivity and weaker buffers reduce the region’s attractiveness on a risk-adjusted basis. That said, selective opportunities remain. The Malaysian ringgit stands out, supported by resilient external balances, diversified exports and a key role in the global semiconductor supply chain, combined with credible policy and relatively lower vulnerability to the oil shock.

Local rates: caution amid uncertainty

Local rates remain an area under close monitoring and one we have actively managed throughout the recent volatility. We reduced duration sharply when the oil shock triggered a broad VaR-driven adjustment across EM markets, before selectively rebuilding exposure as curves priced increasingly aggressive tightening scenarios. More recently, however, we have moderated exposure again as oil prices remained above USD100 and several central banks are now expected to begin or resume hiking cycles.

Our focus therefore remains on identifying selective opportunities in markets where real yields remain high, curves are steep and policy credibility provides central banks with some room to avoid overreacting immediately to a supply-driven inflation shock. At the same time, while awaiting greater clarity on the persistence of higher energy prices and the extent of inflation pass-through, we maintain a measured and flexible approach.

This continues to point toward Central and Eastern Europe (CEE), South Africa and Brazil. In CEE, valuations increasingly reflect inflation risks, while political developments are becoming more supportive (see Hungary below). South Africa offers one of the steepest curves in the EM universe alongside high real yields and a gradually improving political and fiscal backdrop. Brazil remains particularly compelling, with nominal yields close to 14%, elevated real rates and sufficient policy credibility to allow the easing cycle to resume once inflation uncertainty recedes.

Asia remains the counterpoint. Lower carry, higher energy sensitivity and weaker buffers make the region less attractive on a risk-adjusted basis, although selective opportunities remain.

Hungary – on the path to euro accession

Hungary’s political reset has revived a medium-term euro-convergence narrative. A more pro-EU government should help unlock EU funds, lower risk premia and strengthen fiscal credibility.

In the near term, the economy remains exposed to the energy shock, which is likely to push inflation higher and keep the National Bank of Hungary (NBH) cautious. The central bank has adopted a data-dependent stance, reflecting uncertainty around energy prices and domestic price controls, which may delay the start of an easing cycle.

However, these headwinds appear cyclical rather than structural. As external pressures ease, improving policy credibility, potential EU fund inflows and a stronger currency backdrop should support a compression of risk premia, particularly at the long end of the curve, allowing Hungarian rates to outperform ahead of any formal progress toward euro adoption.

Risk management: preserving convexity

None of this means ignoring the downside. March highlighted how quickly EM can de-risk when oil, rates, and geopolitics move in tandem. Protection remains embedded in the portfolio. We increased CDS/CDX hedges during the escalation phase, only partially reducing them as markets stabilised, and have recently added back exposure as markets retraced part of the March sell-off.

With around 25% protection still in place, the objective is not to neutralise beta, but to preserve convexity: protecting capital in tail scenarios, retaining dry powder, and maintaining flexibility across hard currency, local rates, and FX.

The recent oil shock has not derailed the EM cycle, but it has changed its nature. Stronger fundamentals continue to provide resilience, yet the environment is becoming more complex and differentiated. As broad beta gives way to dispersion, returns will increasingly be driven by carry, fundamentals and country selection. In this context, maintaining exposure remains justified, but with a greater emphasis on selectivity and active allocation.

Carmignac Portfolio EM Debt

Carmignac Portfolio EM Debt A EUR Acc

- Recommended minimum investment horizon

- 3 years

- Risk indicator*

- 3/7

- SFDR - Fund Classification**

- Article 8

*Risk Scale from the KID (Key Information Document). Risk 1 does not mean a risk-free investment. This indicator may change over time. **Sustainable Finance Disclosure Regulation (SFDR) 2019/2088. The SFDR classification of the Funds may change over time.

Main risks of the fund

Fees

- Entry costs

- 2.00% of the amount you pay in when entering this investment. This is the most you will be charged. Carmignac Gestion doesn't charge any entry fee. The person selling you the product will inform you of the actual charge.

- Exit costs

- We do not charge an exit fee for this product.

- Management fees and other administrative or operating costs

- 1.41% of the value of your investment per year. This estimate is based on actual costs over the past year.

- Performance fees

- 20.00% when the share class overperforms the Reference indicator during the performance period. It will be payable also in case the share class has overperformed the reference indicator but had a negative performance. Underperformance is clawed back for 5 years. The actual amount will vary depending on how well your investment performs. The aggregated cost estimation above includes the average over the last 5 years, or since the product creation if it is less than 5 years.

- Transaction Cost

- 0.34% of the value of your investment per year. This is an estimate of the costs incurred when we buy and sell the investments underlying the product. The actual amount varies depending on the quantity we buy and sell.

Performance

| Carmignac Portfolio EM Debt | +0.6 | +7.5 | +3.7 | +14.3 | −9.4 | +3.2 | +9.8 | +28.1 | −10.5 | +0.8 |

| Reference Indicator | +0.7 | +8.6 | +4.4 | +8.9 | −5.9 | −1.8 | −5.8 | +15.6 | −1.5 | +0.4 |

| Carmignac Portfolio EM Debt | +5.4% | +3.6% | +4.9% |

| Reference Indicator | +6.6% | +3.4% | +2.5% |

Source: Carmignac at 30 Apr 2026.

Past performance is not necessarily indicative of future performance. Performances are net of fees (excluding possible entrance fees charged by the distributor). The Fund presents a risk of loss of capital.

Reference Indicator: 50% JPM GBI-EM Global Diversified Composite index + 50% JPM EMBI Global Diversified Hedged index

MARKETING COMMUNICATION. Please refer to the KID/KIID/prospectus of the Fund before making any final investment decisions. This document is intended for professional clients.

This document may not be reproduced, in whole or in part, without prior authorisation from the management company. It does not constitute a subscription offer, nor does it constitute investment advice. The information contained in this document may be partial information and may be modified without prior notice. The Management Company can cease promotion in your country anytime. Investors have access to a summary of their rights in French, English, German, Dutch, Spanish, Italian at the following link (paragraph 5 “Summary of investor rights”): https://www.carmignac.com/en/regulatory-information. The decision to invest in the promoted fund should take into account all its characteristics or objectives as described in its prospectus. The Funds are common funds in contractual form (FCP) conforming to the UCITS Directive under French law. Carmignac Portfolio refers to the sub-funds of Carmignac Portfolio SICAV, an investment company under Luxembourg law, conforming to the UCITS Directive. The reference to a ranking or prize, is no guarantee of the future results of the UCITS or the manager. Past performance is not necessarily indicative of future performance. Performances are net of fees (excluding possible entrance fees charged by the distributor). The return may increase or decrease as a result of currency fluctuations, for the shares which are not currency-hedged. Reference to certain securities and financial instruments is for illustrative purposes to highlight stocks that are or have been included in the portfolios of funds in the Carmignac range. This is not intended to promote direct investment in those instruments, nor does it constitute investment advice. The Management Company is not subject to prohibition on trading in these instruments prior to issuing any communication. The portfolios of Carmignac funds may change without previous notice. Access to the Funds may be subject to restrictions with regard to certain persons or countries. The Funds may not be offered or sold, directly or indirectly, for the benefit or on behalf of a U.S. person, according to the definition of the US Regulation S and/or FATCA. The Funds present a risk of loss of capital. The risk, fees and ongoing charges are described in the KIDs/KIIDs (Key Information Document/Key Investor Information Document). The Funds' respective prospectuses, KIDs/KIIDs, NAV and annual reports are available at www.carmignac.com, or upon request to the Management Company. The KIDs/KIIDs must be made available to the subscriber prior to subscription.

- Portugal: The Funds are registered with the Comissão do Mercado de Valores (CMVM). The Funds’ respective prospectuses, KIDs and annual reports are available at www.carmignac.com/pt-pt. The KIDs must be made available to the subscriber prior to subscription.

- Spain, Carmignac Portfolio EM Debt refers to the sub-funds of Carmignac Portfolio SICAV, an investment company under Luxembourg law, conforming to the UCITS directive. The Fund is registered with the Spanish National Securities Market Commission under number Carmignac Portfolio 392.

- Switzerland, the Funds’ respective prospectuses, KIDs and annual reports are available at www.carmignac.com/en-ch or through our representative in Switzerland, CACEIS (Switzerland), S.A., Route de Signy 35, CH-1260 Nyon. The paying agent is CACEIS Bank, Montrouge, succursale de Nyon / Suisse, Route de Signy 35, 1260 Nyon. The KIDs must be made available to the subscriber prior to subscription.

- United Kingdom: This document was prepared by Carmignac Gestion, Carmignac Gestion Luxembourg or Carmignac UK Ltd.

- Belgium: This document has not been submitted to FSMA for validation. It is intended for professionals only. This communication is published by Carmignac Gestion S.A., a portfolio management company approved by the Autorité des Marchés Financiers (AMF) in France, and its Luxembourg subsidiary Carmignac Gestion Luxembourg, S.A., an investment fund management company approved by the Commission de Surveillance du Secteur Financier (CSSF). “Carmignac” is a registered trademark. “Investing in your Interest” is a slogan associated with the Carmignac trademark. This document does not constitute advice on any investment or arbitrage of transferable securities or any other asset management or investment product or service. The information and opinions contained in this document do not take into account investors’ specific individual circumstances and must never be interpreted as legal, tax or investment advice. The risks and fees are described in the KIDs (Key Information Documents). The prospectuses, KIDs, the net asset-values and the latest (semi-) annual management reports may be obtained, free of charge, in French or in Dutch, from the management company (tel. +352 46 70 60 1) or by consulting its website or www.fundinfo.com. These materials may also be obtained from Caceis Belgium S.A., the financial service provider in Belgium, at the following address: avenue du port, 86c b320, B-1000 Brussels. In case of subscription to a fund subject to Article 19bis of the Belgian Income Tax Code (CIR92), the investor will have to pay, upon redemption of his or her shares, a withholding tax of 30% on the income (in the form of interest, or capital gains or losses) derived from the return on assets invested in debt claims. Distributions are subject to withholding tax of 30% without income distinction. In case of subscription in a French investment fund (fonds commun de placement or FCP), you must declare on tax form, each year, the share of the dividends (and interest, if applicable) received by the Fund. Any complaint may be referred to complaints@carmignac.com or CARMIGNAC GESTION - Compliance and Internal Controls - 24 place Vendôme Paris France or on the website www.ombudsfin.be.

CARMIGNAC GESTION - 24, place Vendôme - F-75001 Paris - Tél : (+33) 01 42 86 53 35. Investment management company approved by the AMF -Public limited company with share capital of € 13,500,000 - RCS Paris B 349 501 676.

CARMIGNAC GESTION Luxembourg - City Link - 7, rue de la Chapelle - L-1325 Luxembourg - Tel : (+352) 46 70 60 1. Subsidiary of Carmignac Gestion. Investment fund management company approved by the CSSF. Public limited company with share capital of € 23,000,000 - RCS Luxembourg B 67 549.