The Price of Resilience

Six weeks on, markets stay afloat amid uncertainty largely supported by upbeat earnings expectations.

![[Management Team] [Author] Thozet Kevin](https://carmignac.imgix.net/uploads/NextImage/0001/18/%5BManagement-Team%5D-Thozet-Kevi.png?auto=format%2Ccompress&fit=fill&w=3840)

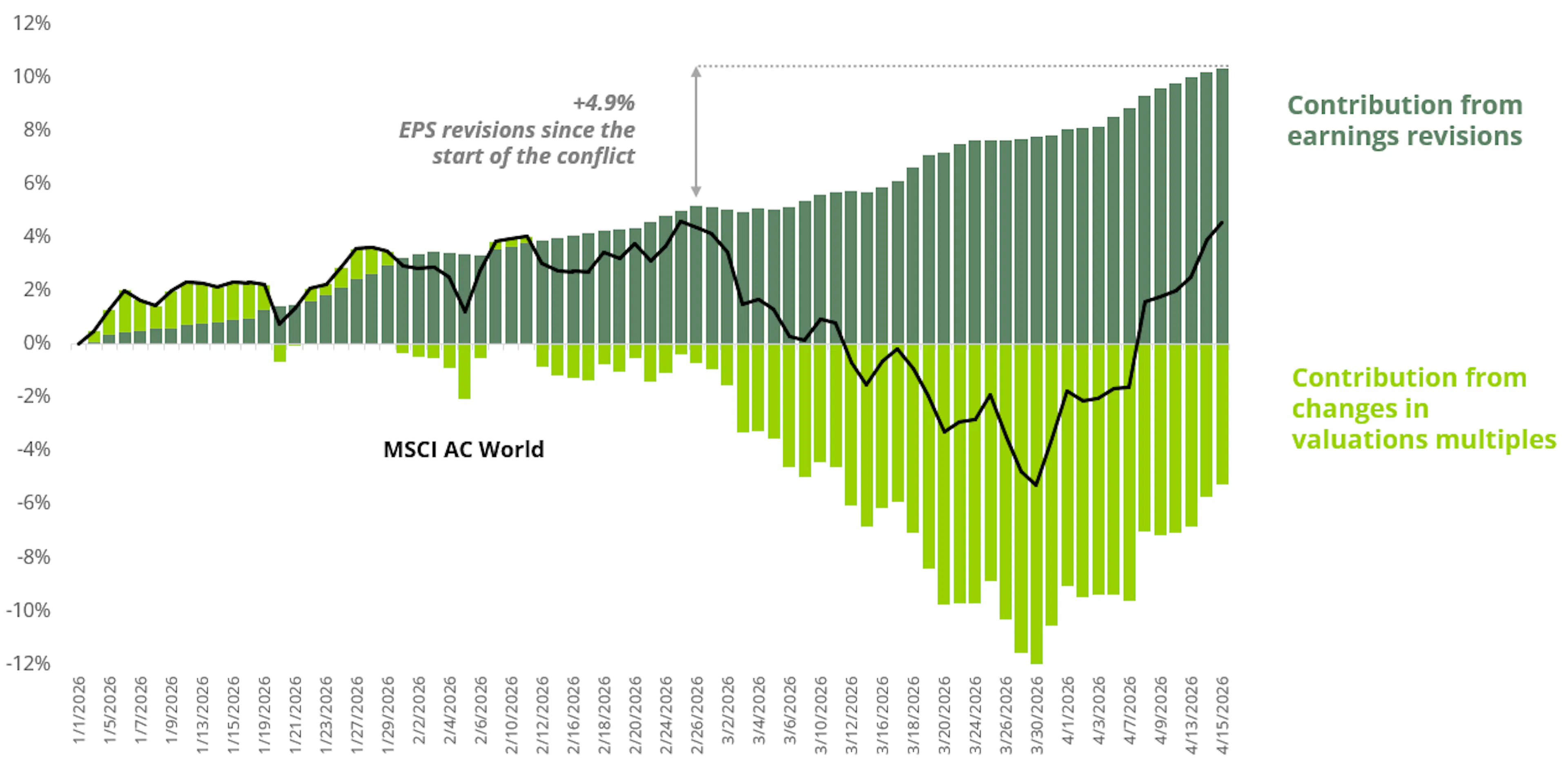

Analysis of MSCI AC World Performance: Impact of Earnings and Valuations

Source: Carmignac, Bloomberg, April 16, 2026.

Six weeks into the Middle East conflict, the resilience of equity markets is striking. After a short-lived pullback, major indices have largely recovered their losses and, in some cases, have even risen above their pre-Iran-war levels. Should this be seen as unwarranted complacency, or as a rational reflection of underlying corporate fundamentals?

Looking more closely at the forces shaping global equity performance helps unravel this apparent paradox. Valuations have not fuelled the advance - on the contrary, multiples have generally edged lower, while dividends have made only a modest contribution. The market rebound is therefore largely attributable to earnings momentum and the robustness of profit growth. Since the outbreak of the Iranian conflict, earnings growth expectations for 2026 have been lifted by over 4 percentage points, to around +20% for global equities for this calendar year.1 This upgrade goes a long way in explaining why markets have remained so resilient despite the uncertain backdrop. These optimistic earnings expectations stand in contrast to a more demanding macro environment characterised by tighter financial conditions, higher interest rates driven by elevated inflation, slowing economic activity, and rising cost pressures, all while margins are already near peak levels.

Markets have seen through the dynamics at play: the surge in earnings expectations is overwhelmingly driven by the energy sector, where forecasts have jumped by more than 35% amid the rebound in oil and gas prices.1 The sector alone accounts for the vast majority of upward Earnings per share (EPS) revisions - and in Europe and Japan, even more than the total increase. A similar dynamic is at play in the materials sector. The technology sector, particularly in the US, continues to enjoy upward revisions, with earnings now expected to grow by around 15% this year, some 6 percentage points higher than at the end of February.1 Companies in the sector are reaping the full benefits of the AI-driven investment cycle, though it remains unclear whether the rise in energy costs has been fully factored in.

By contrast, expectations for consumer and industrial sectors have been revised downward. Rising fuel prices act as a drag on household purchasing power and put pressure on corporate margins. That said, the scale of these downgrades has so far remained relatively contained.

At this stage, the energy shock is perceived as strong enough to materially support sector profits, yet not significant enough to disrupt the broader economic momentum - an assessment that points to a fairly confident, if not optimistic, market stance.

This is where the balance could tip. A downside scenario for markets would emerge from a severe negative supply shock to growth, driven by disruptions caused by the closure of a key maritime route through which 10% to 15% of global seaborne trade flows, compounded by a broad pass-through of higher oil prices across the entire pricing chain. In essence, this would set the stage for a stagflationary outcome. Conversely, a more bullish outcome would see valuations revert toward their (already optimistic) pre-war levels (rising from around 17x to 20x forward earnings). Such a re-rating would likely be driven by a swift resolution of the conflict and a less forceful monetary tightening than currently anticipated, as the drag on growth materialises with a lag. On the basis of current earnings expectations, this would point to further upside of roughly 10% for equity markets.1