Emerging markets are defined by high dispersion, structural inefficiency and information asymmetry. For active managers, these are features that can be exploited. For passive investors, they are a problem that an index fund cannot solve.

Emerging markets delivered their strongest annual return since 2017 in 2025. The headline figure was impressive but what lay beneath could be more instructive.

Korea surged 97% in US dollar terms, South Africa rose 73%, Mexico gained 50% and Brazil 40%. Meanwhile, Saudi Arabia, Indonesia, Argentina and the Philippines all posted negative returns for the year. The same asset class in the same calendar year, but outcomes separated by more than 100 percentage points1.

That dispersion is not a quirk of 2025 but a common characteristic of emerging markets as an asset class. And it is the most straightforward argument against passive exposure: buying the index means buying all of it, the leaders and the laggards, without the ability to distinguish between them.

What passive emerging market exposure actually gives you

Emerging market indices are constructed by market capitalisation, which means they systematically overweight whatever has already performed well and underweight what has not yet been recognised. By the time a company becomes large enough to warrant meaningful index weight, much of its return has already been captured by those who identified it earlier. In a sense, the passive investor arrives late.

According to Naomi Waistell, co-fund manager of FP Carmignac Emerging Markets: "Performance benchmarks are really backward looking barometers of performance rather than telling us about how we want to position for the future."

The construction problem runs deeper than timing. Passive strategies in emerging markets include state-owned enterprises whose objectives often diverge from those of minority shareholders, companies with governance ratings at the bottom of the scale and businesses on exclusion lists for weapons manufacturing, coal extraction or regulatory violations.

An index fund cannot screen any of these out but an active manager can and arguably must.

The inability to respond when an investment case changes is equally costly. When Samsung Electronics failed to obtain Nvidia certification for its most advanced memory chips, its competitive position in the high-bandwidth memory market deteriorated materially but an index fund continued to hold the stock at its market-cap weight.

An active manager who identified the shift in competitive dynamics could exit the position and redeploy into SK Hynix, which had the technological lead and Nvidia’s qualification. And when Samsung obtained the certification active managers could then reinitiate a position in the stock. That was a real-life example that drove some of FP Carmignac Emerging Markets’ recent outperformance.

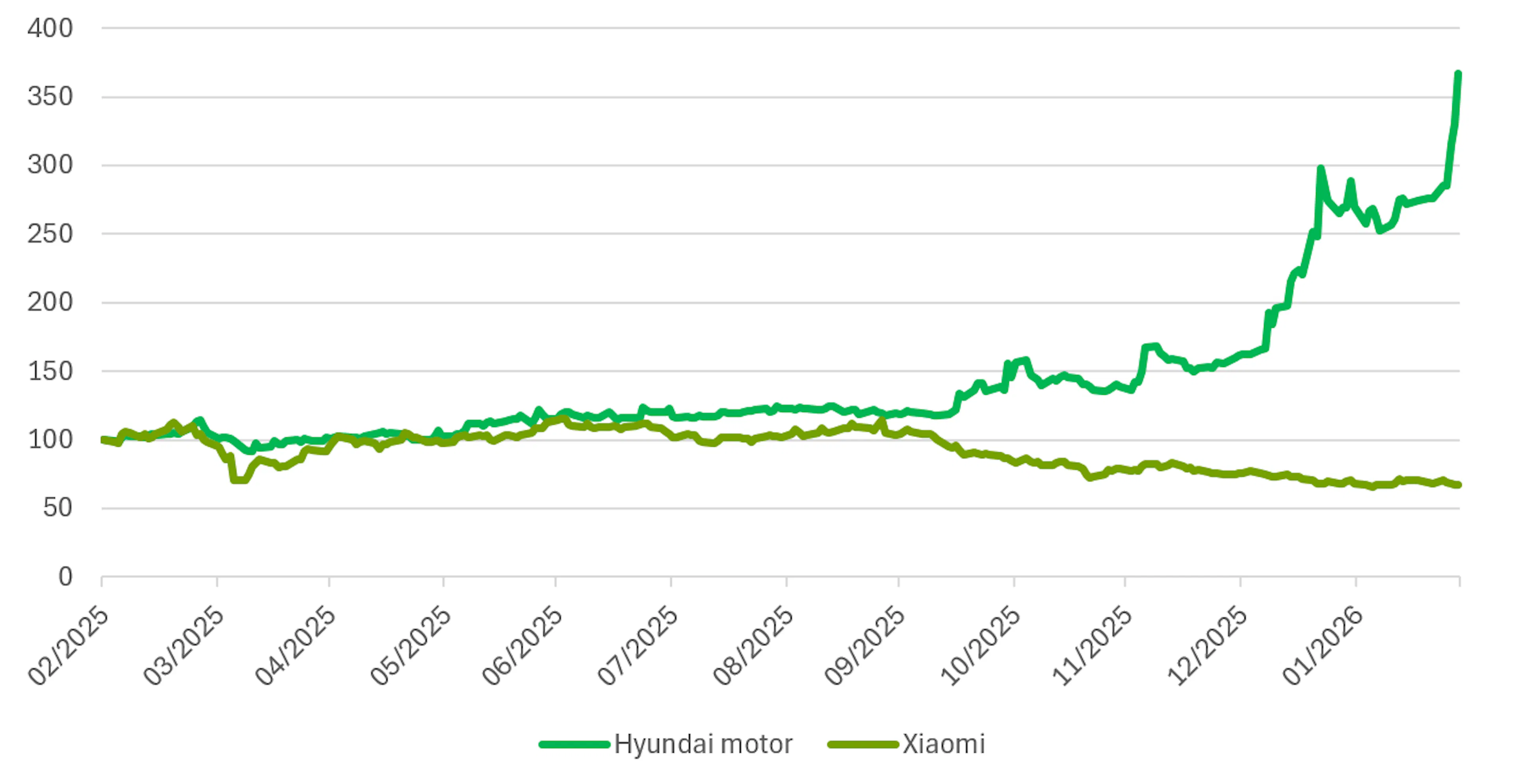

A similar dynamic can be observed in the automotive sector. In emerging market indices, Xiaomi has rapidly become one of the largest auto-related weights following the market’s enthusiasm around its entry into electric vehicles. From a passive perspective, its growing market capitalisation automatically translates into a higher index allocation.

However, an active approach leads to a different conclusion. Rather than following index weights, we prefer companies where fundamentals and long-term competitive advantages appear stronger. In this case, we favour Hyundai. Beyond its established automotive business, Hyundai is investing heavily in robotics through its participation in Boston Dynamics, a technological capability that we believe could meaningfully enhance productivity and strengthen its competitive positioning over time.

The performance divergence illustrates the value of this approach. Over the rolling twelve months to the end of February 2026, Hyundai — which we hold in the portfolio — delivered a return of +267%, while Xiaomi declined by -33% over the same period.

This type of dispersion highlights why fundamental research and active decision-making matter in emerging markets: the largest weight in the index is not necessarily the most compelling investment opportunity.

Why emerging markets specifically reward active management

The conditions that make passive strategies attractive in developed markets, namely high liquidity, standardised disclosure, efficient price discovery and relatively uniform governance, are substantially less prevalent in emerging markets. Information asymmetry is higher, financial statements are sometimes non-standardised and local dynamics require on-the-ground knowledge that cannot be derived from a screen.

Waistell describes these conditions not as obstacles but as sources of opportunity: "Emerging markets are volatile by nature. They always have been. And sometimes we can actually use that volatility, the extra inefficiencies in emerging markets to our advantage when we're investing."

FP Carmignac Emerging Markets co-fund manager Xavier Hovasse added: "In emerging markets, there's a lot of volatility and sometimes stocks go up way too much. So, we take that opportunity to trim or they go down way too much, which is an opportunity to buy more at a very good price."

The cost of getting country and sector allocation wrong in emerging markets is also substantially higher than in developed markets, where broad economic trends tend to lift all boats to a similar degree. In emerging markets, country selection alone can swing returns by a substantial margin, as 2025 demonstrated.

Hovasse, who is Carmignac’s Head of Emerging Equities, said: "When you invest in emerging markets, both top down and bottom up are very important. In terms of the chronology, you start with the top-down thinking. You need to find the best countries, the best sectors, the best businesses, and only after that you need to try to find the best vehicles to play that."

The shift from beta to alpha

The 2025 emerging market equity rally was primarily beta-driven. As macro conditions improved and investor sentiment turned positive, price/earnings multiples expanded across the asset class. Broad exposure worked because everything was rising.

The next phase could be different. With emerging markets now trading at around 12.5x forward 2026 earnings, elevated relative to recent history, further multiple expansion is less certain. Emerging market equities are forecast to deliver mid-to-high-teens EPS growth in 2026 and returns from here are more likely to be determined by which companies actually deliver the expected earnings than by a broad re-rating of the asset class2.

Waistell elaborated: "A weaker US dollar, historically high real rates and stable inflation provide EM central banks with room to gradually ease monetary policy, creating meaningful tailwinds. However, we are entering a phase of rising dispersion, where returns are likely to be driven more by earnings growth than multiple expansion, making selectivity more important than index exposure."

How Carmignac approaches the opportunity

FP Carmignac Emerging Markets is a direct counterpoint to passive exposure. The portfolio holds 35-45 stocks, selected through a combination of top-down country and sector analysis and rigorous bottom-up stock picking. Active share stood at 80% as of end-March 2026, meaning the portfolio is substantially different from the reference indicator it is measured against.

The fund managers also work closely with a dedicated Front Office Risk Management team to better understand the portfolio’s sensitivity to different market variables, for example by assessing its sensitivity to oil prices, US real rates and to a value vs growth bias. Understanding these underlying sensitivity and bases of the fund enables the fund managers to make more informed investment decisions and adjust the portfolio if needed and illustrates the value added by active management compared with passive strategies.

Sustainability is integrated as an investment discipline rather than a constraint. As Waistell explained: "We think that sustainability is actually value accretive and alpha seeking in its own right. We're just putting more information, more fundamental analysis into stock prices upfront."

Since the fund's launch in May 2019, it has returned +99%3 against a reference indicator return of +58%4, net of fees as at the end of March 2026.

Waistell concludes: “The other thing that's key is to have a clear process and follow that process through the long term. That avoids being buffeted by some of the short-term factors. Yes, we can be agile if we need to and make bold decisions when that's called for, but ultimately what we're trying to do is drive the best risk-adjusted returns.”

1Source: Bloomberg, MSCI, 31/12/2025.

2Sources: Carmignac, CLSA Research, Bloomberg, 12/01/2026.

3Performance of FP Carmignac Emerging Markets A GBP ACC.

4Reference indicator: MSCI EM NR index.

FP Carmignac Emerging Markets

FP Carmignac Emerging Markets A GBP ACC

- Recommended minimum investment horizon

- 5 years

- Risk indicator*

- 6/7

- SFDR - Fund Classification

- Article -

*Risk Scale from the KIID (Key Investor Information Document). Risk 1 does not mean a risk-free investment. This indicator may change over time.

Main risks of the fund

Fees

- Maximum subscription fees paid to distributors

- -

- Redemption Fees

- -

- Conversion Fee

- -

- Ongoing Charges

- 0.95%

- Management Fees

- 0.87% MAX

- Performance Fees

- -

Footnote

Performance

| FP Carmignac Emerging Markets | +1.1 | +28.9 | +0.9 | +7.2 | −9.5 | −15.6 | +63.0 | +13.6 |

| Reference Indicator | +1.8 | +24.4 | +9.4 | +3.6 | −10.0 | −1.6 | +14.7 | +8.8 |

| FP Carmignac Emerging Markets | +10.7% | +2.1% | +10.5% |

| Reference Indicator | +12.4% | +4.6% | +6.9% |

Source: Carmignac at 31 Mar 2026.

Past performance is not necessarily indicative of future performance. Performances are net of fees (excluding possible entrance fees charged by the distributor). The Fund presents a risk of loss of capital.

Reference Indicator: MSCI EM NR index

Marketing communication. Please refer to the KIID/prospectus of the Fund before making any final investment decisions.

This document was prepared by Carmignac Gestion, Carmignac UK Ltd and/or Carmignac Gestion Luxembourg and is being distributed in the UK by Carmignac Gestion Luxembourg.

This material may not be reproduced, in whole or in part, without prior authorisation from the Management Company. This material does not constitute a subscription offer, nor does it constitute investment advice. This material has been provided to you for informational purposes only and may not be relied upon by you in evaluating the merits of investing in any securities or interests referred to herein or for any other purposes. The information contained in this material may be partial information and may be modified without prior notice.

Past performance is not necessarily indicative of future performance. Performances are net of fees (excluding possible entrance fees charged by the distributor). The return may increase or decrease as a result of currency fluctuations, for the shares which are not currency-hedged. Reference to certain securities and financial instruments is for illustrative purposes to highlight stocks that are or have been included in the portfolios of funds in the Carmignac range. This is not intended to promote direct investment in those instruments, nor does it constitute investment advice. The Management Company is not subject to prohibition on trading in these instruments prior to issuing any communication. The portfolios of Carmignac funds may change without previous notice.

Access to the Fund may be subject to restrictions regarding certain persons or countries. The Fund has not been registered under the US Securities Act of 1933. The Fund may not be offered or sold, directly or indirectly, for the benefit or on behalf of a «U.S. person», according to the definition of the US Regulation S and FATCA. The risks, fees and ongoing charges are described in the KIID. The KIID must be made available to the subscriber prior to subscription. The subscriber must read the KIID. Investors may lose some or all their capital, as the capital in the funds are not guaranteed. The Fund’s prospectus, KIID, NAV and annual reports are available at www.carmignac.com, or upon request to the Management Company. The Management Company can cease promotion in your country anytime. Investors have access to a summary of their rights in English at section 5 of "regulatory information page" on the following link: https://www.carmignac.com/en-gb/regulatory-information.

FP Carmignac ICVC (the “Company”) is an Investment Company with variable capital incorporated in England and Wales under registered number 839620 and is authorised by the Financial Conduct Authority (the “FCA”) with effect from 04/04/2019 and launched on 15 May 2019. FundRock Partners Limited is the Authorised Corporate Director (the “ACD”) of the Company and is authorised and regulated by the Financial Conduct Authority. Registered Office: Hamilton Centre, Rodney Way, Chelmsford, England, CM1 3BY, UK (Registered in England and Wales under No 4162989). Carmignac Gestion Luxembourg SA has been appointed as the Investment Manager and distributor in respect of the Company. Carmignac UK Ltd and Carmignac Gestion S.A. have been appointed as sub-Investment Managers of the Company. Carmignac UK Ltd is authorised and regulated by the Financial Conduct Authority (FRN: 984288).

CARMIGNAC GESTION 24, place Vendôme - F-75001 Paris - Tel : (+33) 01 42 86 53 35 Investment management company approved by the AMF Public limited company with share capital of € 13,500,000 - RCS Paris B 349 501 676.

CARMIGNAC GESTION Luxembourg - City Link - 7, rue de la Chapelle - L-1325 Luxembourg - Tel : (+352) 46 70 60 1 Subsidiary of Carmignac Gestion - Investment fund management company approved by the CSSF. Public limited company with share capital of € 23,000,000 - RCS Luxembourg B 67 549.