In today’s environment, investors are increasingly focused on intangible assets that drive long-term performance, such as human capital and intellectual property. Once viewed as a wellness initiative confined to HR, employee mental health is now recognised as a material business issue with direct implications for productivity, retention, risk exposure, and ultimately, share price.

The financial cost of overlooking employee mental health is astonishing. According to the World Health Organization (WHO), mental health illnesses cost the global economy an estimated $1 trillion annually in lost productivity1. In the U.S. employers lose approximately $47.6 billion each year due to mental health-related absenteeism and presenteeism2, while broader job stress accounts for up to $300 billion in annual costs3. In the UK, this figure stands at £51 billion annually4, equivalent to nearly 2% of the country’s GDP5.

When employees are disengaged or struggling, customer service deteriorates, deadlines are missed, and innovation falls. These outcomes can lead to slower, reduced profitability, and heighten operational risks, ultimately impacting company valuation.

For investors seeking sustainable alpha, understanding how companies manage employee satisfaction and well-being is crucial. Beyond reputational considerations, poor mental health is a material financial matter as higher employee turnover, reduced engagement, and rising healthcare costs, erode margins and compress valuation multiples.

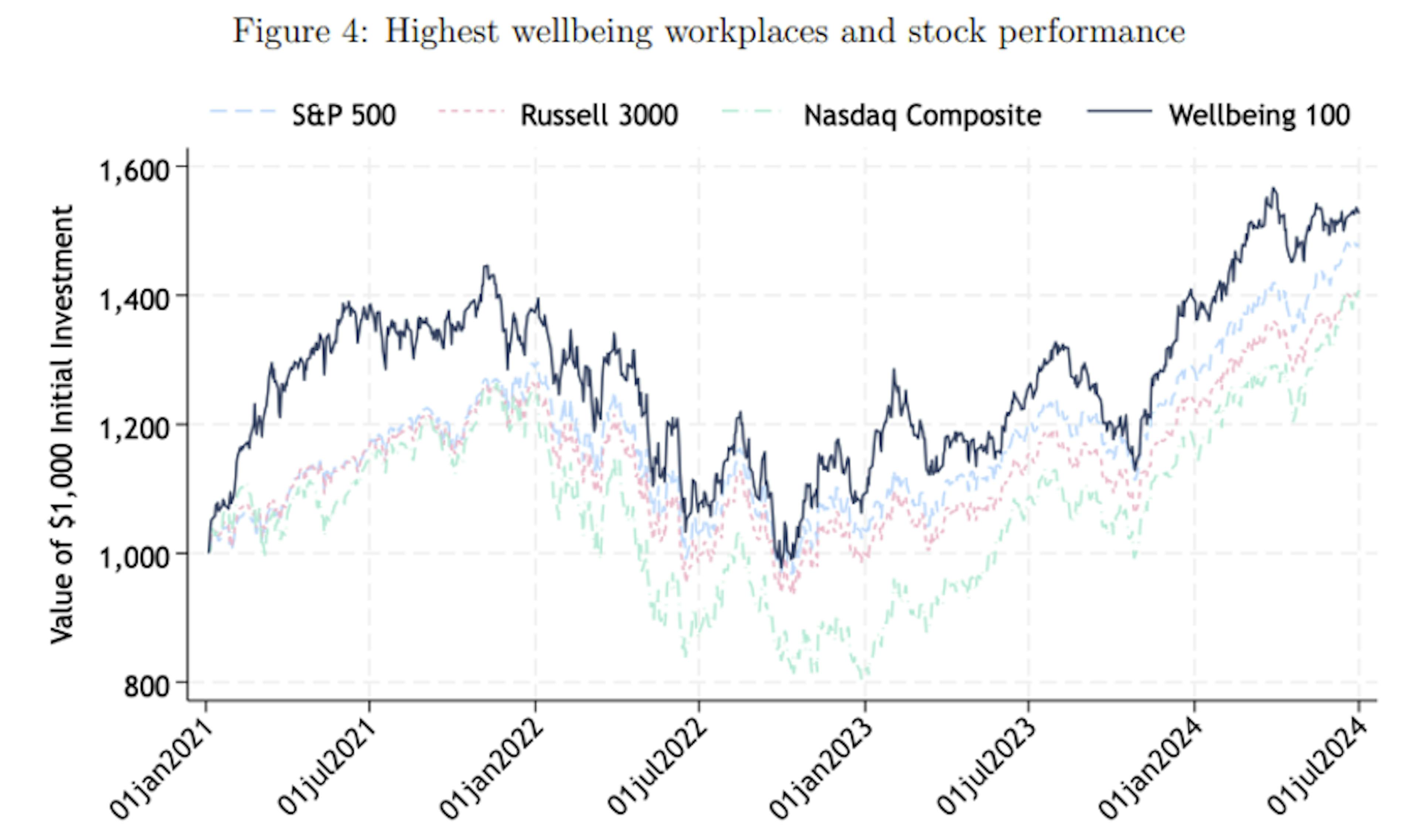

Employee mental health and company/share price performance

The body of evidence that employee mental health drives a company’s financial performance is growing.

Oxford University found that happier employees are 13% more productive6. Gallup reports that highly engaged teams achieve 23% higher profitability7. And Alex Edman found that the ‘100 Best Companies to Work For in America’ delivered stock returns that beat their peers by 2.1% to 3.5% per year over a 26-year period8. In contrast, fear in the workplace harms retention and creativity9. Of course, employee happiness alone is insufficient in driving growth and innovation; a balanced approach promoting wellbeing and positive motivation with moderate challenge creates the most effective work environment10.

The mental health of a workforce is not just a signal of management quality but also operational resilience. These are key factors that influence investor confidence in a company.

The financial and reputational cost of neglecting employee mental health

While positive employee mental health can improve company performance, the reverse is also true, with some company scandals even leading to legislative change.

A wave of employee suicides at France Télécom (now Orange) in the early 2000’s was linked to humiliating management practices, leading to executive imprisonment11 and 2% share price drop at the time12. At Dentsu, the suicide of 24-year-old Matsuri Takahashi after working 100 hours overtime per month, resulted in the company president resigning and new national labour laws restricting overtime in Japan13. Another famous example is Foxconn employee suicides in China in 2010, which triggered intense media and public scrutiny of Foxconn’s working conditions and labour practices14. This resulted in a net loss of $218.3 millions in 2010 due to increased wage bills and welfare costs, leading to a share price derating15.

Stewardship in action: engagement insights on employee mental health

In line with our stewardship priorities, in 2025 we initiated engagements with a cross-section of portfolio companies to evaluate how they manage employee mental health, and to assess alignment between commitments and practices.

Our engagement targeted 10 companies across financial services, consumer goods, and technology sectors, across international holdings in our funds.

Our findings revealed recurring themes:

- Leadership: All companies spoke about the importance of leadership normalising discussions about mental health.

- Support: All companies has at least one form of support for employees, such as an Employee Assistance Programme (EAP).

- Gaps between policy and practice: All firms had wellness statements and initiatives but most lacked targets for implementation and improvement.

- Hybrid working: Most companies spoke about the importance of hybrid working and flexibility for employee mental health.

- Measurement challenges: Companies struggled to quantify the mental health impact on productivity or cost, and the depth of questions on the topic in employee engagement surveys varies greatly.

Best practice case studies

Roche:

- Every business site conducts psycho-social risk assessments.

- Targets set in place to continuously improve mental health support.

- Mandatory employee mental health training for managers.

- Frequent employee surveys – in addition to the annual Global Employee Opinion Survey, the company conducts shorter, more frequent surveys throughout the year to quickly gauge employee sentiment and address any emerging issues.

Mastercard:

- Medical director in the company, who reports to HR and is designed to help employees.

- Collaboration with other organisations on the best ways to integrate mental health initiatives.

- Has a specific crisis service, provided through the employee relations team.

- Dedicated quiet zones and meditation zones in the office.

The investor lens - why mental health is material

As investment managers, our primary obligation is to assess risk-adjusted returns. Mental health fits within this framework both as a downside risk and an investment opportunity. The quality of a company’s approach to mental wellbeing can offer critical insights into its governance, risk culture, and operational foresight.

Investors can take several steps to evaluate mental health as part of a broader ESG integration strategy:

- Engage with companies on their mental health policies, resources, and employee feedback mechanisms during earnings calls or stewardship meetings.

- Request disclosures on metrics such as absenteeism rates, mental health-related insurance claims, turnover data, and employee engagement surveys.

- Integrate wellbeing indicators into human capital due diligence - particularly in sectors reliant on intellectual property, service delivery, or creative output.

- Support shareholder resolutions that advocate for mental health policies or broader human capital transparency.

Conclusion

In an investment climate increasingly shaped by long-term value creation, employee mental health is emerging as a signal of business quality. It should not be mistaken for a corporate charity initiative. It is a material factor with tangible implications for productivity, culture, and returns.

Mental wellbeing is not just good ethics, it is good economics. We believe the companies that will outperform in the coming decade will be those that treat their workforce as an asset to be nurtured, not a cost to be managed. This is particularly important as we usher in an era of humans collaborating with artificial intelligence. It is time for investors to ask hard questions, demand better data, and recognise companies that prioritise the mental health of the employees.

1Mental health at work.

2The Economic Cost of Poor Employee Mental Health.

3Financial Costs of Job Stress | Total Worker Health for Employers | CPH-NEW | Research | UMass Lowell.

4Poor mental health costs UK employers £51 billion a year for employees | Deloitte UK.

5Country Cassette GDP by Country.

6https://www.ox.ac.uk/news/2019-10-24-happy-workers-are-13-more-productive

7https://www.gallup.com/workplace/285674/improve-employee-engagement-workplace.aspx

8Does the stock market fully value intangibles? Employee satisfaction and equity prices.

9Fear and work performance: A meta-analysis and future research directions - ScienceDirect.

10https://selfdeterminationtheory.org/wp-content/uploads/2023/10/2021_VandenBroeckEtAl_Beyond.pdf

11France Télécom suicides: Three former bosses jailed - BBC News.

12France Telecom suicides could impact business-analysts | Reuters.

13https://hr.asia/featured-news/new-labour-laws-to-address-japans-culture-of-overworking/

14Apple, H-P Investigating Foxconn's Steps to Deal With Suicides - WSJ.

15Foxconn (Hon Hai Precision Industry) (2317.TW) - Stock price history.

Marketing Communication. Please refer to the KID/prospectus of the fund before making any final investment decisions. This document is intended for professional clients.

The decision to invest in the promoted fund should take into account all its characteristics or objectives as described in its prospectus. This material may not be reproduced, in whole or in part, without prior authorisation from the Management Company. This material does not constitute a subscription offer, nor does it constitute investment advice. This material has been provided to you for informational purposes only. The information contained in this material may be partial information and may be modified without prior notice. Reference to certain securities and financial instruments is for illustrative purposes to highlight stocks that are or have been included in the portfolios of funds in the Carmignac range. This is not intended to promote direct investment in those instruments, nor does it constitute investment advice. The Management Company is not subject to prohibition on trading in these instruments prior to issuing any communication. The portfolios of Carmignac funds may change without previous notice.

Access to the Funds may be subject to restrictions regarding certain persons or countries. The Funds are not registered for retail distribution in Asia, in Japan, in North America, nor are they registered in South America. Carmignac Funds are registered in Singapore as restricted foreign scheme (for professional clients only). The Funds have not been registered under the US Securities Act of 1933. The Funds may not be offered or sold, directly or indirectly, for the benefit or on behalf of a «U.S. person», according to the definition of the US Regulation S and FATCA. The Management Company can cease promotion in your country anytime.

The risks, fees and ongoing charges are described in the KID. The KID must be made available to the subscriber prior to subscription. The Funds’ prospectus, KIDs, NAV and annual reports are available at www.carmignac.com, or upon request to the Management Company.

Investors have access to a summary of their rights in French, English, German, Dutch, Spanish, Italian at section 5 of "regulatory information page" on the following link:

https://www.carmignac.com/en_US/regulatory-information.

Carmignac Portfolio Xperience refers to a sub-fund of Carmignac Portfolio SICAV, an investment company under Luxembourg law, conforming to the UCITS Directive.

Carmignac Gestion - 24, place Vendôme - 75001 Paris. Tel: (+33) 01 42 86 53 35 – Investment management company approved by the AMF. Public limited company with share capital of € 13,500,000 - RCS Paris B 349 501 676.

Carmignac Gestion Luxembourg - City Link - 7, rue de la Chapelle - L-1325 Luxembourg. Tel: (+352) 46 70 60 1 – Subsidiary of Carmignac Gestion - Investment fund management company approved by the CSSF. Public limited company with share capital of € 23,000,000 - RCS Luxembourg B 67 549.