Quality in Europe: Are we at a turning point?

![[Management Team] [Author] Denham Mark](https://carmignac.imgix.net/uploads/NextImage/0001/18/%5BManagement-Team%5D-Denham-Mark.png?auto=format%2Ccompress&fit=fill&w=3840)

Mark Denham, fund manager of the FP Carmignac ICVC European Leaders Fund, explains why he thinks now is the right time to invest in quality stocks in Europe.

Over recent years, European Quality equities have undergone a significant de-rating despite resilient and in some cases improving fundamentals. Rising interest rates, macro uncertainty, and a rotation toward cyclicals have driven multiple compression, leaving valuations increasingly disconnected from the strength and consistency of their earnings profiles. As a result, valuation multiples have compressed, often to levels that appear disconnected from the structural strength and earnings resilience these companies continue to demonstrate.

We believe this dislocation is unlikely to persist and we intrinsically think this de-rating may have already reached a floor. The current macro uncertainties as well as the fundamental strength of these companies could be setting the stage for a potential inflection point in European quality equities. Here we believe FP Carmignac ICVC European Leaders is well positioned to demonstrate the robustness of its stock selection which has fared well historically.

In a re-rating environment, we believe bottom-up stock selection is essential to identify companies where the disconnect between fundamentals and valuations is most pronounced enabling us to differentiate between genuine structural winners with resilient earnings and those where multiple compression may be justified, ensuring more effective capture of both earnings growth and valuation upside.

In this context, despite a lagging performance of +8.88% vs +10.15% for the MSCI Europe ex UK since January 20251, FP Carmignac ICVC European Leaders is deliberately positioned to capture this re-rating opportunity. By focusing on companies with a durable competitive advantage, strong pricing power, and robust cash flow generation, the fund is well aligned to benefit from a rotation in market leadership back toward quality.

1. From de-rating to re rating?

While we have seen the worst performing periods for European quality in 2024 and 2025in over a decade, we do not see these driven by weaker fundamentals but instead an outsized rally in lower quality companies.

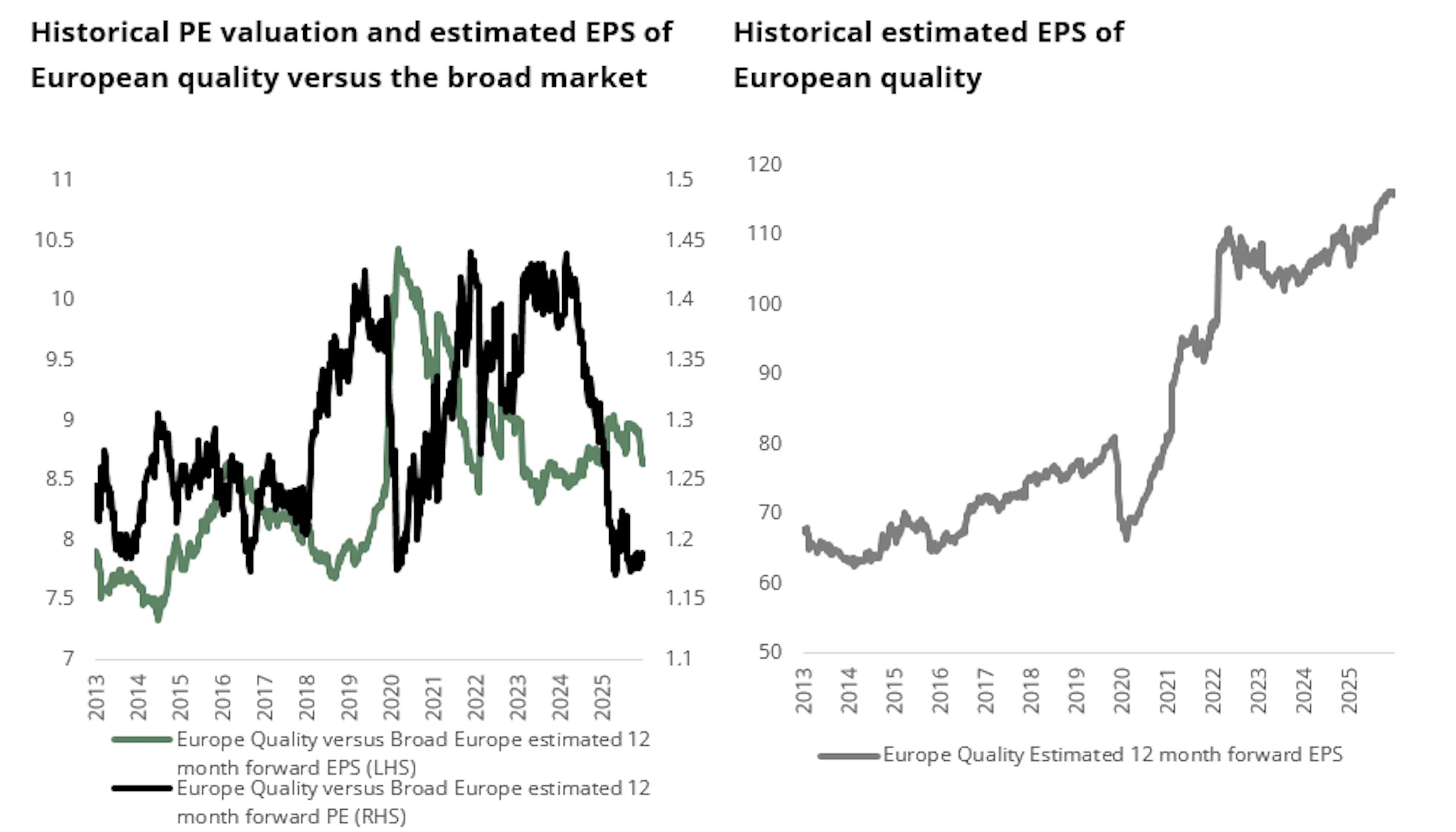

MSCI Europe Quality is trading at the lower end of its historical valuation range in relative terms to the broader European market. This can be explained by the most recent rerating of non-quality EPS since 2020, primarily seen in balance sheet financials (banks and insurance), energy and materials as well as more broadly cyclical sectors. Nevertheless, despite a weaker relative estimated EPS estimates for quality, we see this stabilising and in absolute terms, growing. This multiple compression has been broad-based, indicating a systematic derating rather than a deterioration in fundamentals, with profitability, balance sheet strength and earnings visibility remaining robust. As such, we see the current dislocation as being increasingly unsustainable. If earnings momentum continues to build, valuations are likely to re-rate, particularly given how compressed multiples have become.

2. A mispriced opportunity

The derating has been driven by a pronounced rotation into cyclicals and domestic stocks, as well as the impact of higher real rates on long-duration equities.

We see earnings resilience and the strength of company balance sheets as the main reasons why Quality as mispriced perhaps even more so in uncertain environments.

A. Earnings resilience

European Quality equities continue to demonstrate a structurally more resilient earnings profile across market cycles. Both forward estimates and realised earnings highlight greater stability, visibility, and consistency relative to the broader market, underpinned by strong business fundamentals.

We see several important patterns that demonstrate quality's earnings resilience:

- Growth trajectory: Quality shows strong upward momentum in forward earnings estimates. This can notably be seen from end 2020 to mid 2022, as well as in 2025, highlighting the visibility and resilience of its earnings profile.

- Lower drawdowns of earnings during stress periods: During market downturns and earnings revisions cycles, notably during the China and commodities slowdown in 2015-2016 and during the Covid Shock in 2020, Quality experienced smaller drawdowns in earnings estimates compared to the broader market. This reflects the defensive characteristics of high-quality companies, underpinned by stronger pricing power, recurring revenue streams, and more resilient end-market demand, which collectively dampen earnings volatility during periods of macro stress, as mentioned above.

- Faster recovery: Following periods of earnings estimate compression, such as the ones mentioned above (2016 and 2020), Quality stocks demonstrated quicker stabilization and recovery in forward earnings expectations. This again indicates stronger earnings visibility and operational resilience, enabling high-quality companies to re-anchor growth trajectories more quickly as macro headwinds subside.

B. Profitability resilience

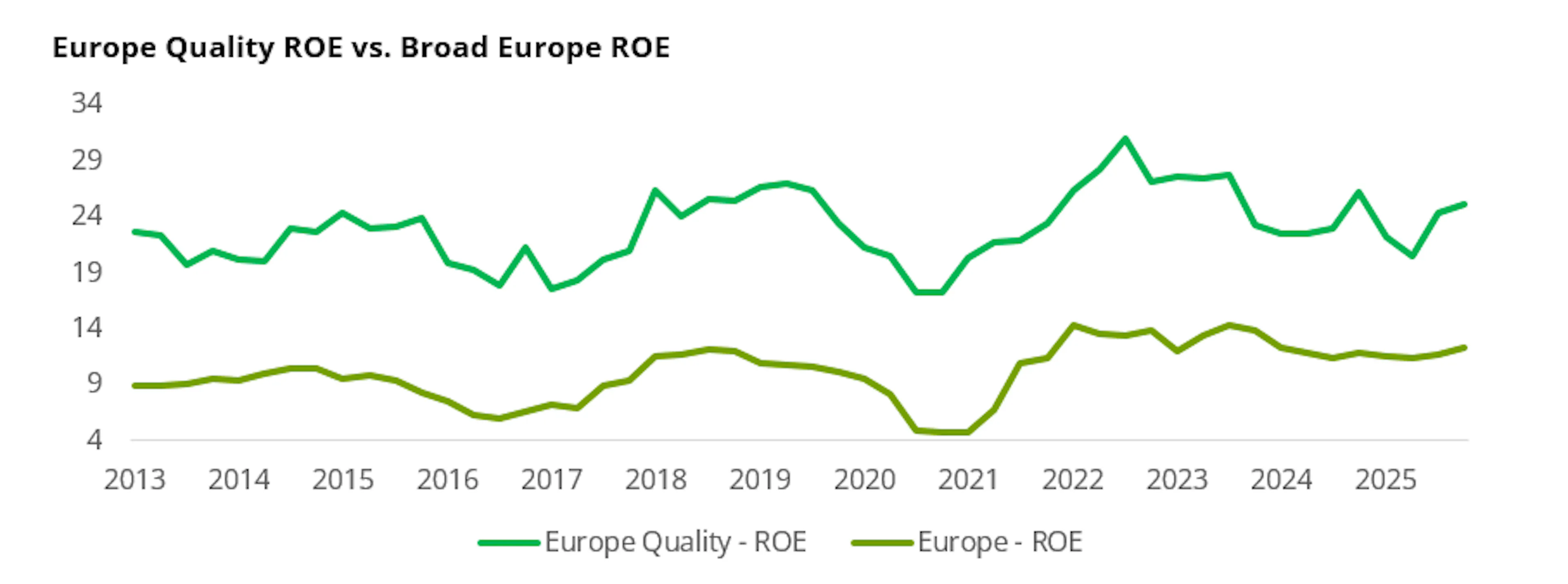

MSCI Europe Quality has consistently outperformed the broader market in return on equity, maintaining levels around twice as high over 2021–2026 (24.9% vs 12.4%)2, highlighting its structural profitability advantage. This premium has persisted across cycles, with Quality peaking at higher levels and showing stronger resilience during the 2023–2024 compression period, with more durable profitability and downside protection. Looking ahead, while both the broad market and Quality are expected to recover, we expect Quality to maintain its structural ROE premium.

Quality also exhibits a structural profitability advantage, with net margins around 47% higher than the broader market2, reflecting stronger pricing power and operational efficiency. During periods of margin compression, Quality experienced less severe declines, maintaining a clear premium and demonstrating its defensive characteristics. Looking ahead, margins are expected to recover to 14.9% by 2026 versus 10.8% for the broader market2, supported by superior pricing power and cost discipline.

Overall, we believe that Quality currently offers an attractive entry point, with improving fundamentals not yet reflected in valuations. The combination of stabilising-to-improving EPS and depressed multiples creates a favourable asymmetry, with scope for both earnings delivery and multiple expansion to drive returns. This resilience in profitability, rooted in the structural characteristics of Quality companies, supports their ability to navigate cycles and downturns, yet remains underappreciated by the market, resulting in a clear mispricing.

3. Why the tide is turning for quality

C. Uncertainty favouring quality

The European macroeconomic backdrop is currently characterised by elevated uncertainty, which has been emphasized by the current situation in the Middle East. Stabilised monetary policy, which may not remain stable for long, lingering energy market volatility and wider geopolitical tensions keep these uncertainties at the heart of market movements. Simultaneously, fiscal constraints and uneven industrial activity across the region continue to cloud the outlook. This environment has contributed to heightened dispersion in earnings expectations and increased sensitivity of cyclical sectors to macro shocks, reinforcing a more fragile and unpredictable growth profile across the broader market. With these risks of potential stagflation, we can imagine greater risks to the broader European market which is less tilted towards companies with stronger balance sheets and earnings resilience. In this context, Quality companies are structurally better positioned to navigate uncertainty thanks to their strong pricing power, recurring revenue streams, and high barriers to entry, which support earnings visibility and margin resilience even in more volatile conditions enhancing their ability to absorb external shocks without compromising long-term growth. If earnings miss expectations in the lower quality segment of the market, we expect quality stocks demonstrating this resilience to re rate.

As macro risks persist, these attributes become increasingly valuable. In this environment, investors are expected to become more discriminating, favouring companies with strong visibility, rewarding businesses capable of delivering consistent cash flows and navigating weaker demand without material earnings volatility. This shift back toward fundamentals should position Quality stocks to outperform as earnings certainty becomes increasingly scarce and valuable.

D. EU infrastructure spend tailwind

The acceleration of infrastructure investment across Europe, from EU programmes such as NextGenerationEU, InvestEU and REPowerEU to national initiatives like Germany’s €500bn fund, provides a structurally supportive backdrop for Quality companies in areas that tend to be more cyclical by nature. Spending is concentrated in long-duration areas such as electrification, grids, rail, and digital infrastructure, where high barriers to entry favour established players. Crucially, these projects are underpinned by multi-year order books and long-term contracts, enhancing revenue visibility and extending earnings duration. This allows for these more cyclical Quality companies to lock in cash flows with greater certainty and reduces sensitivity to short-term macro and cyclical fluctuations.

This reinforces the structural, rather than cyclical, nature of the current investment cycle. Unlike traditional stimulus, European infrastructure spend is policy-driven and anchored in long-term priorities. The combination of sustained demand, high visibility, and lower cyclicality of these policies should support a gradual re-rating of these Quality companies, as markets increasingly recognise the durability of their growth and earnings profiles.

From a bottom-up standpoint selection is key in order to identify these higher quality stocks that we think will deliver solid returns both at a Europe wide level as well as at a local market level, in the case of Germany. Looking for quality stocks within these more cyclical sectors has been one of the areas of focus for us since 2025 to enable us not only to diversify our portfolio, but also to position these holdings for the medium-term benefits they can bring to the strategy.

E. Spillover of ai capex into Europe

The rapid expansion of AI-related capital expenditure, driven by US hyperscalers, is creating significant second-order effects across global industrial and technology value chains, with Europe emerging as a key beneficiary. While the bulk of direct investment is concentrated in data centres and compute infrastructure, the enabling ecosystem is highly global, and Europe holds critical positions in several upstream segments. European companies are particularly well represented in semiconductor equipment, power management, electrification, and industrial automation, areas that are essential to scaling AI infrastructure. ASML, for example, is uniquely positioned to benefit from the global spillover of AI-driven capex, given its critical role in enabling advanced semiconductor production, reinforcing its structural growth profile. As AI deployment accelerates, demand extends beyond compute to include grids, cooling, connectivity, and energy-efficient systems, reinforcing Europe’s strategic role in this ecosystem. We can see this in industrial names within the electrification theme, with companies like Schneider Electric and Prysmian being well positioned to benefit from this spillover through increased demand for data centre infrastructure, power distribution and cable solutions.

This dynamic is particularly supportive for European companies, which tend to dominate these specialised, high-value segments. Their roles are crucial in the supply chain where switching costs are high and alternatives are scarce allowing them to capture sustained demand from long-duration AI investment cycles. Moreover, much of this demand is secured through multi-year order books and strategic partnerships, enhancing earnings visibility and reducing cyclicality. As a result, this reinforces the structural growth profile of these companies, supporting both earnings resilience and potential multiple re-rating. Exposure to AI-driven infrastructure demand provides an additional layer of durable, non-cyclical growth for high-quality businesses.

4. Translating conviction into positioning

Within FP Carmignac ICVC European Leaders, our investment approach is centred on identifying high-quality companies across the region and across sectors, with a focus on capturing the valuation dislocation currently observed between Quality and the broader market. We aim to avoid concentration risk and instead build a diversified portfolio of businesses that exhibit resilient earnings profiles and superior long-term growth characteristics.

In the current environment, our approach allows us to selectively allocate capital to the most compelling opportunities. We focus on companies where the gap between valuation and intrinsic quality is most pronounced. By combining disciplined fundamental analysis with a long-term investment horizon, we seek to capture both earnings compounding and potential multiple re-rating, positioning the portfolio to benefit as markets gradually re-align with underlying fundamentals.

Two areas we see benefitting from this reversal are Healthcare and stock exchanges, within Financials, where we hold 25% and 5% respectively3. Healthcare has been de rated despite robust fundamentals and structural growth. European healthcare valuations were particularly impacted by developments in the US healthcare market, including political uncertainty, drug pricing concerns and regulatory headlines, which weighed indiscriminately on global investor sentiment. As these US specific fears fade and market leadership broadens, the disconnect between resilient earnings and compressed valuations creates scope for multiple expansion. Similarly with stock exchanges, their capital light, high ROIC business models have been de rated despite structurally resilient earnings. Valuations were further compressed by fears that AI could disintermediate trading, pricing and market data revenues, concerns we see as overstated given exchanges’ control of regulated market infrastructure and proprietary data. In an environment of higher volatility and macro uncertainty, exchanges benefit from rising trading activity and demand for risk management, supporting earnings visibility as investor multiples normalise.

Over the past year we have opportunistically been adding to companies we like that we saw as being mispriced relative to their fundamentals. Whether in more cyclical quality names or names historically held in the fund, we have been building these positions to better capture the opportunity ahead of us.

This can be illustrated through specific company examples4, where identifiable catalysts support both the durability of earnings and the potential for valuation re-rating.

Alcon is a global leader in eye care, providing surgical equipment, intraocular lenses and vision care products such as contact lenses. We view it as a mispriced defensive grower, with the market overly focused on near-term margin pressures despite strengthening fundamentals and consistent mid-single digit organic growth of 5–7%. The company missed their targets twice last year with sales and revenues slightly below expectations both in Q2 and Q4 , but we see that more from softness in demand and external headwinds such as a weaker dollar and tariffs, rather than a collapse in fundamentals. However, looking forward, we see normalisation in margin pressures, increase in volume of procedures and stronger contribution from new product cycles.

Overall, the business benefits from structural growth drivers (ageing demographics, rising procedure volumes), recurring revenues, and strong cash generation (€1.7bn FCF with FCF yield expected to grow from 3.7% to 7.4% by 2030). This supports high-single digit EPS growth and strong earnings visibility. Despite this, the stock trades on 23x forward P/E, with multiples near the bottom of its 5 year range significantly below its 29x average, highlighting a disconnect between valuation and fundamentals.

In a macro environment marked by, Alcon’s low cyclicality and high earnings visibility position it as a high-conviction “resilient growth” compounder, with scope for both continued EPS delivery and multiple re-rating as investors rotate back toward defensive quality.

RELX, the global leader in data-driven analytics and decision tools, provides mission-critical data, workflow solutions and insights across markets. Fundamentally, the group combines high visibility and recurring revenues with structural tailwinds, through strong execution with sustained margin expansion, robust cash generation (£3.3bn FCF with 5.8% yield), and earnings growth (9% adjusted operating profit growth in 2025, targeting continued acceleration).

Despite this, RELX trades on 19.4x forward P/E, below its 31x 5-year average, reflecting market concerns around AI disruption concerns which have weighed on the share price, as investors questioned the durability of its content-driven model and the risk of commoditisation. However, we believe these concerns are overstated. Rather than being disrupted, RELX is well positioned to be a key enabler of AI, leveraging its proprietary data, domain expertise and embedded workflows to deliver high-value, trusted analytics. Its datasets are difficult to replicate, and the integration of AI into its platforms should enhance product functionality, deepen customer relationships and support pricing power.

5. Conclusion

In an environment of increased dispersion, we believe investors will increasingly refocus on durability, cash flow visibility, and risk adjusted returns.

The de-rating of European Quality stocks is not driven by weak fundamentals, but by non-fundamental factors. They are not cheap because their underlying performance has deteriorated, but because they have temporarily fallen out of favour. With earnings resilience intact, margins stabilising, and valuations disconnected from underlying business strength, we see the turning point approaching, making this a compelling re entry point for long term investors willing to look beyond short term macro noise. In this context, we have positioned FP Carmignac ICVC European Leaders to benefit from this long-awaited reversal, which we believe will allow the strategy to demonstrate the strength of its stock selection, as evidenced in the past.

1Source: Carmignac 30/04/2026 for B GBP ACC share class.

2MSCI, Bloomberg, 31/03/2026.

3As at 31/03/2026. Reference to certain securities and financial instruments is for illustrative purposes. The portfolio is subject to change without notice.

4Reference to certain securities and financial instruments is for illustrative purposes only and the portfolio is subject to change without notice.

FP Carmignac European Leaders

FP Carmignac European Leaders B GBP ACC

- Recommended minimum investment horizon

- 5 years

- Risk indicator*

- 6/7

- SFDR - Fund Classification

- Article -

*Risk Scale from the KIID (Key Investor Information Document). Risk 1 does not mean a risk-free investment. This indicator may change over time.

Main risks of the fund

Fees

- Maximum subscription fees paid to distributors

- -

- Redemption Fees

- -

- Conversion Fee

- -

- Ongoing Charges

- 0.55%

- Management Fees

- 0.47% MAX

- Performance Fees

- -

Footnote

Performance

| FP Carmignac European Leaders | −5.4 | +6.2 | +7.1 | +14.3 | −14.5 | +14.3 | +27.5 | +18.5 |

| Reference Indicator | +2.1 | +26.2 | +1.9 | +14.8 | −7.6 | +16.7 | +7.5 | +8.8 |

| FP Carmignac European Leaders | +4.2% | +3.0% | +8.9% |

| Reference Indicator | +10.7% | +8.8% | +9.7% |

Source: Carmignac at 30 Apr 2026.

Past performance is not necessarily indicative of future performance. Performances are net of fees (excluding possible entrance fees charged by the distributor). The Fund presents a risk of loss of capital.

Reference Indicator: MSCI Europe ex UK NR index

MARKETING COMMUNICATION

This document may not be reproduced, in whole or in part, without prior authorisation from the Investment Manager. This document does not constitute a subscription offer, nor does it constitute investment advice.

This material may not be reproduced, in whole or in part, without prior authorisation from the Management Company. This material does not constitute a subscription offer, nor does it constitute investment advice. The information and opinions contained in this document do not consider investors’ specific individual circumstances. This material is not intended to provide, and should not be relied on for, accounting, legal or tax advice. The information contained in this material may be partial information and may be modified without prior notice. The information is expressed as of the date of writing and is derived from proprietary and non-proprietary sources deemed by Carmignac to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by Carmignac, its officers, employees or agents.

Reference to certain securities and financial instruments is for illustrative purposes to highlight stocks that are or have been included in the portfolios of funds in the Carmignac range. This is not intended to promote direct investment in those instruments, nor does it constitute investment advice. The Management Company is not subject to prohibition on trading in these instruments prior to issuing any communication. The portfolios of Carmignac funds may change without previous notice. Risk Scale from the KID/ KIID. Risk 1 does not mean a risk-free investment. This indicator may change over time. The recommended investment horizon is a minimum and not a recommendation to sell at the end of that period.

FP Carmignac ICVC (the “Company”) is an Investment Company with variable capital incorporated in England and Wales under registered number 839620 and is authorised by the Financial Conduct Authority (the “FCA”) with effect from 4 April 2019 and launched on 15 May 2019. FundRock Partners Limited is the Authorised Corporate Director (the “ACD”) of the Company and is authorised and regulated by the FCA. Registered Office: Hamilton Centre, Rodney Way, Chelmsford, England, CM1 3BY, UK; Registered in England and Wales with number 4162989. Carmignac Gestion Luxembourg SA has been appointed as the Investment Manager and distributor in respect of the Company. Carmignac UK Ltd (Registered in England and Wales with number 14162894) has been appointed as a sub-Investment Manager of the Company and is authorised and regulated by the Financial Conduct Authority with FRN:984288.

Access to the Company may be subject to restrictions with regard to certain persons or countries. The Company is not registered in North America, in South America, in Asia nor is it registered in Japan. The Company has not been registered under the US Securities Act of 1933. The Company may not be offered or sold, directly or indirectly, for the benefit or on behalf of a U.S. person, according to the definition of the US Regulation S and/or FATCA. The Company presents a risk of loss of capital. The risks and fees are described in the KIID (Key Investor Information Document). The Company’s prospectus, KIIDs and annual reports are available at www.carmignac.com or upon request to the Investment Manager. The KIID must be made available to the subscriber prior to subscription. This material was prepared by Carmignac Gestion Luxembourg SA or Carmignac UK Ltd and is being distributed in the UK by the Investment Manager.

Carmignac Gestion, 24, place Vendôme - 75001 Paris. Investment management company approved by the AMF. Public limited company with share capital of € 13,500,000 - RCS Paris B 349 501 676

Carmignac Gestion Luxembourg, City Link - 7, rue de la Chapelle - L-1325 Luxembourg. Subsidiary of Carmignac Gestion - Investment fund management company approved by the CSSF. Public limited company with share capital of € 23,000,000 - RCS Luxembourg B 67 549